OpenAI has the governance structure of a unicorn - it does not exist

OpenAI built its brand on responsible governance. The internal record says otherwise. A web of 400 portfolio companies, a venture fund Sam owned without the board's knowledge, and a pattern of deals that keep landing in his favor.

Note from Dan: this article long, apologies, I tried and tried to cut it down, but there's too much good material and I couldn't without impacting the analysis. Apologies for the long read, let me know what you think in the comments.

Everyone remembers the WeWork story, the $47 billion valuation that collapsed eighty percent in forty days once the S-1 made the governance legible, Adam Neumann walking away with $1.7 billion. What usually gets glossed over is the specific machinery that made all of it possible. Neumann held supervoting shares at ten votes each, personally owned buildings that WeWork leased from him to the tune of $110 million in future rent commitments by 2018, trademarked the word "We" and charged his own company $5.9 million for the privilege, and had his wife Rebekah written into the governance documents as someone who would help select his successor if he died, which is the kind of clause you write when nobody in the room is being paid to say no. The board, which included experienced people from Benchmark and SoftBank, nodded through all of it for years, right up until that six-week window in 2019 when the governance structure became publicly legible and the whole thing fell apart.

The business does not have to be fake for the governance to kill it, and the governance does not have to be obviously broken for it to fail when it matters. What has to happen is that the gap between what the founder stands to personally gain and what the company claims to exist for becomes visible all at once, and when it does, it turns out that every safeguard people had been pointing to was decorative rather than structural. Which brings us to OpenAI, a company that has spent years making the strongest public case of any AI lab for why this technology needs careful, mission-driven governance, and whose own internal record already demonstrates that it cannot govern itself.

The Frontman

Neumann had to perform his way into $47 billion because performance was all he had to trade on, and Altman is in many ways his inverse: he walked into the OpenAI CEO chair in 2019 with the rolodex of someone who had spent a decade running Y Combinator, the kind of person who did not need to perform his way into anything. Which makes the fact that he has spent the last three years volunteering for every stage OpenAI could put him on all the more telling: the Senate testimony tour, the global head-of-state roadshow, the White House podium alongside Trump and Ellison and Son announcing Stargate. Altman is not a natural performer in the way Neumann was, but he is a willing one, and OpenAI has given him the biggest stage in technology to perform on.

Both companies needed a face who could stand in front of the mission and convert belief into capital, and in both cases the person doing the standing has his personal interests woven through the company he leads in ways that become more obvious the longer anyone bothers to look.

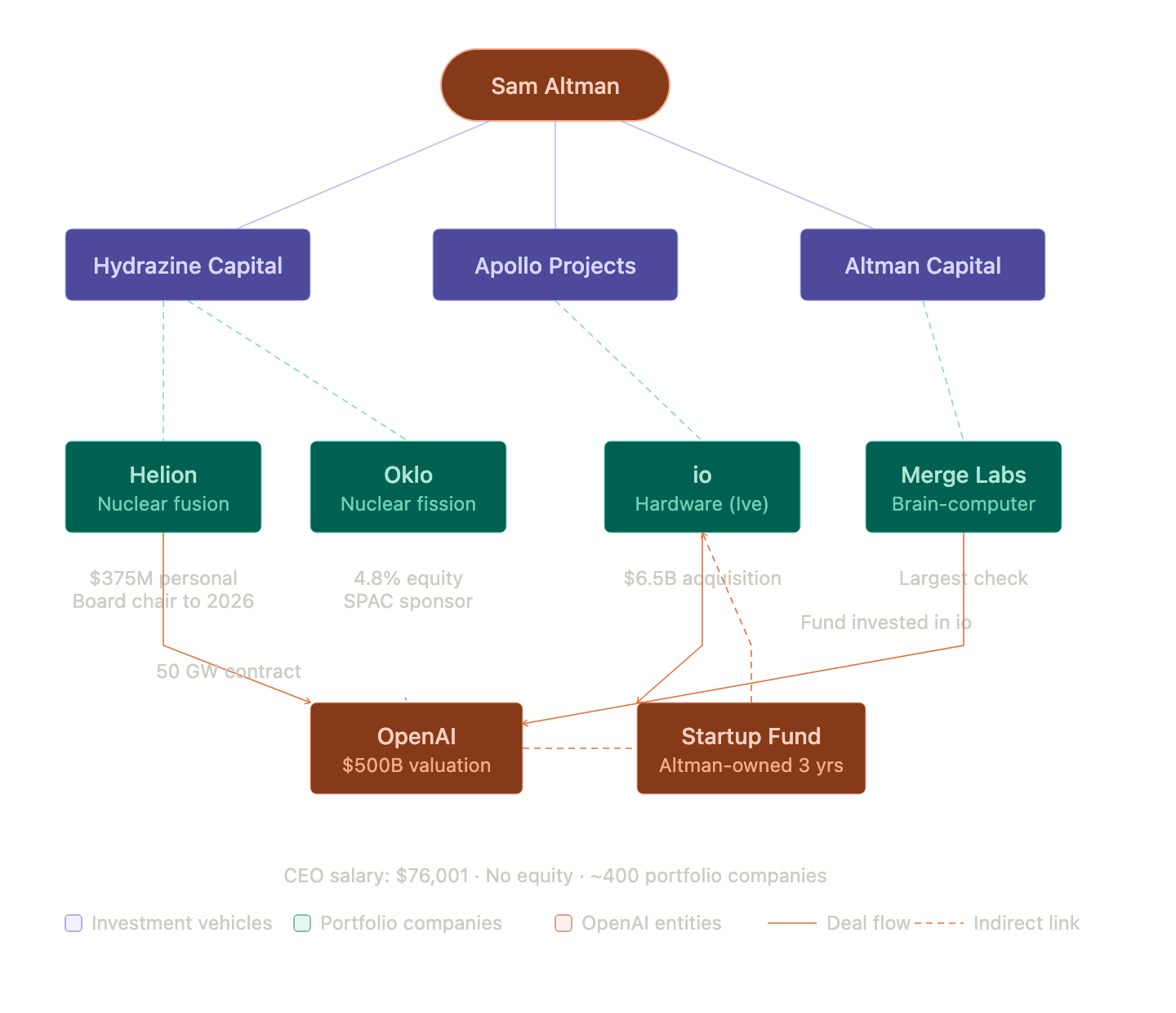

Altman's posture for years has been that he takes no equity in OpenAI and earns a salary of $76,001, which is true, and which has served as a rhetorical shield against conflict-of-interest questions for about as long as the questions have been asked. What the zero-equity line obscures is that his financial interest in OpenAI's decisions is enormous, just distributed across roughly four hundred companies held through Hydrazine Capital (the family office he co-founded with his brother Jack), Apollo Projects, and Altman Capital. The Wall Street Journal reported in April 2026 that Altman has pledged shares in these portfolio companies as collateral on a JPMorgan line of credit he uses to fund further investments, a structure that essentially lets the portfolio feed itself, growing on its own momentum like a loyalty card that earns points you can spend on more loyalty cards. Neumann owned buildings and a trademark. Altman's version is three investment vehicles, a credit facility, and a web of portfolio companies that either sell to OpenAI, buy from OpenAI, or are being positioned to do one or the other soon.

Why Recusal Doesn't Work

OpenAI's standard response to any conflict-of-interest question involving its CEO is that Altman recused himself from the relevant decision, which is the right answer for a CEO with one or two outside investments and a completely inadequate answer for a CEO with four hundred of them. At that scale, recusal is a man locking the front door and leaving every window in the house wide open, then pointing to the lock when someone asks about the security. The best illustration of why it fails is Helion Energy, a nuclear fusion startup that has been promising commercially viable fusion power for years without yet demonstrating that its technology can produce more electricity than it consumes.

Altman has been a Helion shareholder since 2014, put $375 million into it in November 2021, and chaired its board until March 2026, meaning a substantial portion of his net worth sits in a company whose prospects depend on selling electricity to exactly the kind of AI operation OpenAI is building. In January 2025, with Helion falling behind on promised breakthroughs and running short on cash, Altman proposed that OpenAI invest roughly $500 million at a $35 billion valuation, more than six times the previous $5.4 billion, a jump that would have been aggressive for a fusion startup hitting its milestones and was extraordinary for one that wasn't. He was formally recused from the OpenAI decision, but he was also the person who had proposed it, and during the same period he separately asked Masayoshi Son to back Helion while SoftBank was finalizing its own $40 billion investment in OpenAI.

OpenAI ultimately declined the equity investment, which is the fact the company points to when it says the process worked, but OpenAI also signed an agreement giving it the right to purchase up to fifty gigawatts of electricity from Helion by 2035, roughly the output of twenty-five Hoover Dams, and Helion has since cited that contract to prospective investors to help raise money, which lifts the valuation, which lifts the value of Altman's personal stake. So the CEO proposed a deal that would have enriched him, stepped back from the vote, watched the deal come back in a different shape that enriched him anyway, and the governance apparatus waved it through like a security guard checking badges at a building where everyone already knows each other's name.

The Rest of the Iceberg

Helion has the most fresh reporting behind it, but the same pattern, recusal offered as protection, recusal failing to protect, runs through deal after deal if you bother to follow the money.

Oklo, a nuclear fission company Altman took public via his own SPAC in May 2024, is perhaps the most revealing example of what happens when the governance toolbox runs out of tools. Altman remained Oklo's chairman until April 2025, when he stepped down explicitly, per the public filings, to "avoid conflict of interest" and "open up opportunities for future deals between OpenAI and Oklo," which is a sentence worth reading twice: the CEO of OpenAI resigned from a company he had taken public so that OpenAI could do business with it, while retaining a 4.8 percent equity stake that would benefit directly from any deal that followed. This is a referee taking off the jersey, walking to the stands, and continuing to collect his cut of the ticket sales while insisting he has no influence on the game.

The CEO of OpenAI resigned from a company he had taken public so that OpenAI could do business with it, while retaining a 4.8 percent equity stake in Oklo that would benefit directly from any deal that followed.

The io acquisition is where the Startup Fund enters the picture. io was the hardware startup Altman had been working on with Jony Ive for two years, and when OpenAI acquired it in May 2025 for $6.5 billion, Altman reportedly owned no equity in io directly, which has become the standard phrasing. But the OpenAI Startup Fund, marketed from 2021 onward as OpenAI's corporate venture arm, had invested in io in 2024, and OpenAI then bought a 23 percent stake for $1.5 billion before acquiring the rest for $5 billion, meaning every stage of the value flow ran through entities Altman either controlled or co-founded.

And the Startup Fund itself turned out to have been personally owned by Sam Altman for three years without the board's knowledge, a fact that former board member Helen Toner has said was among the triggers for the November 2023 firing. Ownership was transferred to fund manager Ian Hathaway via SEC filing in April 2024, and OpenAI's line is that the arrangement was "temporary" and involved no personal financial interest, which is a bit like saying the person who lived in your spare room rent-free for three years was just visiting. For three years the CEO of OpenAI personally owned a venture fund marketed as OpenAI's, and that fund was investing in companies OpenAI would later acquire at multi-billion-dollar valuations. If this sounds like Neumann's "We" trademark move, that is because it is, at larger scale and with a considerably more forgiving press corps.

Merge Labs, a brain-computer interface company Altman co-founded with Alex Blania, raised a $252 million seed round in January 2026 at an $850 million valuation, with OpenAI writing the largest single check and its own blog post describing Altman's role as "in a personal capacity," which prompted TechCrunch to open its coverage with "Just when you thought the circular deals couldn't get any more circular."

A Pattern, Not an Incident

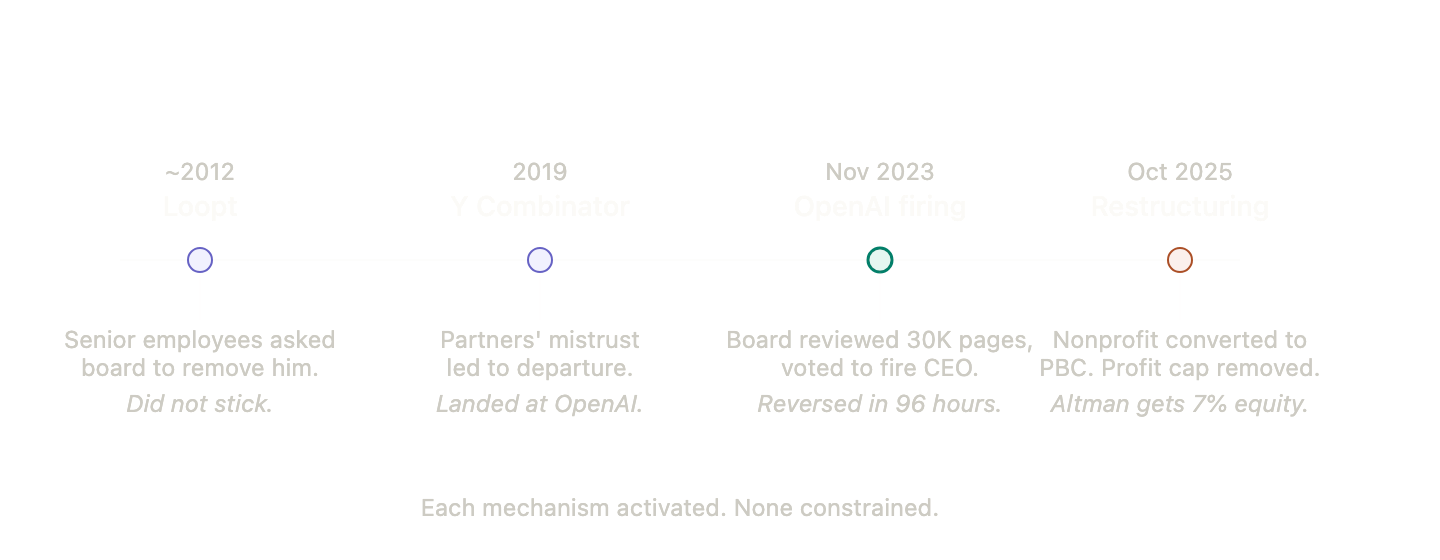

The November 2023 firing was the third time governance mechanisms around Altman had been activated, after earlier episodes at Loopt, where senior employees twice asked the board to remove him as CEO, and at Y Combinator, where partners' mistrust reportedly led to his departure in 2019. Neither attempt stuck, and the OpenAI version was by far the most consequential.

Chief scientist Ilya Sutskever, with input from CTO Mira Murati, compiled a dossier documenting what they described as a pattern of misleading the board. Two executives separately reported what they called "psychological abuse." Altman had told the board that certain products had been approved by a safety panel, and when Helen Toner asked for documentation, only one of three claimed approvals turned out to be real. The board reviewed over thirty thousand pages of material, deliberated, and voted him out.

The governance mechanism did exactly what it was designed to do, and it was then overridden inside ninety-six hours by roughly 700 employees with vested equity and Microsoft as the major commercial partner. Neumann's governance problem was that his supervoting shares made the board unable to fire him. Altman's governance problem is that the board could fire him, did fire him, and got reversed before the week was out, which is the worse outcome, because at least Neumann's board knew it was powerless. The replacement board, chaired by Bret Taylor and including Larry Summers, has never published the conflict-of-interest policy that was supposedly strengthened after the firing.

The Restructuring

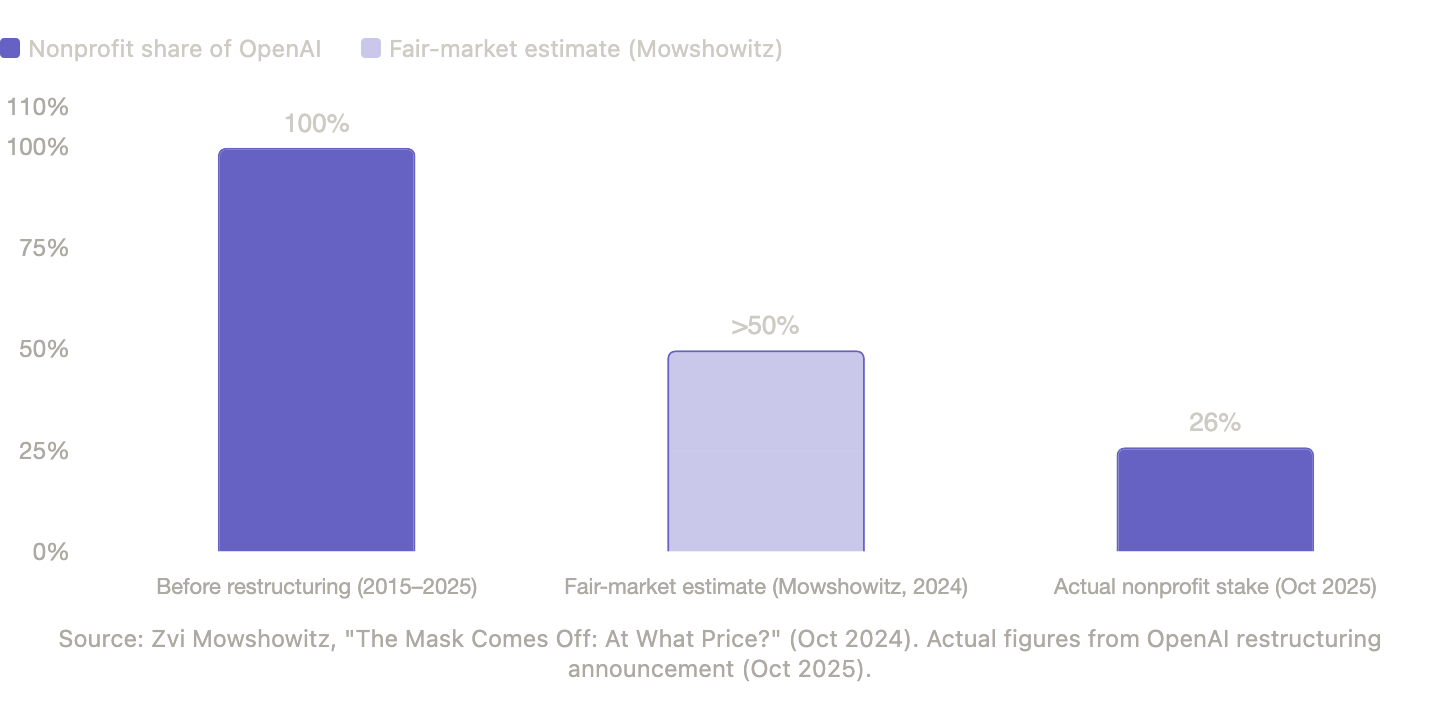

In October 2025 OpenAI completed its restructuring, converting from a capped-profit LLC under a nonprofit into a public benefit corporation, with the nonprofit Foundation holding 26 percent worth around $130 billion, Microsoft holding 27 percent, employees and other investors holding 47 percent, the previous profit cap eliminated, and the whole thing pushed through on a schedule set by SoftBank, whose $40 billion commitment was conditional on the conversion happening by early 2026.

The financial incentives driving OpenAI’s restructuring mirror a broader pattern across corporate America, where companies are using the AI narrative to restructure in ways that reward insiders while the technology itself remains largely unproven at scale.

Rett Wallace, the analyst who read WeWork's S-1 in 2019, called that prospectus "a masterpiece of obfuscation," and OpenAI's "Our Structure" page is written in the same register, the kind of prose that looks rigorous until you try to extract a load-bearing claim from it. The Foundation is described as "positioned to be the single largest long-term beneficiary of OpenAI's success," which is true as stated and concealing as deployed, because Zvi Mowshowitz calculated that a fair-market-value conversion would have given the nonprofit over 50 percent of the shares, not 26 percent. The nonprofit traded away its claim on the upside of AGI itself and somehow came out of the negotiation with a minority stake, which is roughly the equivalent of owning the only well in a desert and agreeing to swap it for a twenty-six percent share in the bottling company.

The standard response to all of this is that the board has been tightened, the conflict policies strengthened, and the Foundation controls the whole edifice with safety veto powers, all of which is true on paper and none of which has survived contact with reality. The board that fired Altman had exactly the mission-first composition people keep asking for and got steamrolled in four days, the new board has never published its conflict policy, and the Helion deal, the Oklo pipeline, and the Merge Labs check all happened anyway. A company that has argued more publicly than any competitor that AI development is too important for ordinary commercial incentives has built a governance structure that bends around its CEO the way water bends around a rock, finding every available path that doesn't require going through the obstacle.

The S-1 Problem

At this point the evidence that OpenAI has a Neumann-style self-dealing problem is overwhelming, just distributed across four hundred companies instead of concentrated in a single S-1 paragraph. Altman has publicly said an IPO is "the most likely path forward," bankers are modeling valuations up to $1 trillion, and the company is sitting on roughly $1.4 trillion in committed infrastructure spend it cannot service without public-market capital. When that S-1 lands, the related-party disclosures will have to list the Helion power contract, the Oklo pipeline, the io acquisition chain, the Merge Labs investment, the Startup Fund arrangement, and whatever else accumulates between now and filing day.

OpenAI has spent years positioning itself as the responsible actor in a field where the other major players are either open-sourcing everything or racing to ship without safety guardrails. If the S-1 makes legible what is already clear from the reporting, that the structure enforces nothing and the mission bends around the CEO's interests the way it has bent at every company he has previously led, then OpenAI will have proved something worse than WeWork ever did. WeWork was a real-estate company that pretended to be a technology company, and the worst consequence of its governance failure was that investors lost money. OpenAI is the company building what it has called the most transformative and potentially dangerous technology in human history, and it has already demonstrated, at every level of its own governance, that it cannot restrain the person making the decisions. The question is not whether the market will eventually notice. The question is what happens in the meantime.

Sources

WeWork and Adam Neumann

- Brown, Eliot and Maureen Farrell. "The Cult of We: WeWork, Adam Neumann, and the Great Startup Delusion." Crown Publishing, 2021.

- "WeWork's Adam Neumann offered package worth up to $1.7 billion to step down from board." CNBC, October 22, 2019. https://www.cnbc.com/2019/10/22/weworks-adam-neumann-to-get-200-million-to-leave-board-report-says.html

- "One Bright Spot From the WeWork Debacle: Turns Out Investors Actually Care About Corporate Governance." Fortune, September 25, 2019. https://fortune.com/2019/09/25/wework-adam-neumann-we-co-corporate-governance-investors/

- "We Company CEO in hot water over being both a tenant and a landlord." TechCrunch, January 16, 2019. https://techcrunch.com/2019/01/16/we-company-ceo-in-hot-water-over-being-both-a-tenant-and-a-landlord/

- "WeWork." Crain's New York Business, April 1, 2019. https://www.crainsnewyork.com/real-estate/wework-ceo-made-millions-leasing-company

Sam Altman's biography, salary, equity and portfolio

- "Sam Altman." Wikipedia, accessed April 2026. https://en.wikipedia.org/wiki/Sam_Altman

- "Sam Altman says dropping out of Stanford wasn't risky." Fortune, September 19, 2024. https://fortune.com/2024/09/19/sam-altman-stanford-dropout-loopt-risks-advice/

- "OpenAI may soon be the most valuable private company, but Sam Altman's net worth won't jolt." Fortune, August 21, 2025. https://fortune.com/2025/08/21/openai-billionaire-ceo-sam-altman-new-valuation-personal-finance-zero-equity-salary-investments/

- "Sam Altman's Investment Web." CB Insights Research, April 7, 2025. https://www.cbinsights.com/research/report/sam-altman-investments/

Helion and the Wall Street Journal reporting

- "Sam Altman's side hustles blur the line between OpenAI's interests and his own." Wall Street Journal via India IPO, April 2026. https://www.indiaipo.in/news/detail/sam-altmans-side-hustles-blur-the-line-between-openais-interests-and-his-own

- "Sam Altman's outside bets raise fresh conflict questions as OpenAI nears IPO." Business Today, April 17, 2026. https://www.businesstoday.in/technology/story/sam-altmans-outside-bets-raise-fresh-conflict-questions-as-openai-nears-ipo-526161-2026-04-17

- "Conflict of Interest Storm Engulfs OpenAI." SL Guardian, April 2026. https://slguardian.org/conflict-of-interest-storm-engulfs-openai-as-sam-altmans-private-deals-face-scrutiny/

- "Nuclear fusion start-up Helion scores $375 million investment from OpenAI CEO Sam Altman." CNBC, November 5, 2021. https://www.cnbc.com/2021/11/05/sam-altman-puts-375-million-into-fusion-start-up-helion-energy.html

- "Sam Altman-backed fusion startup Helion in talks to sell power to OpenAI." TechCrunch, March 23, 2026. https://techcrunch.com/2026/03/23/sam-altman-openai-fusion-energy-board-helion/

The OpenAI Startup Fund

- "Former OpenAI board member explains why CEO Sam Altman got fired before he was rehired." CNBC, May 29, 2024. https://www.cnbc.com/2024/05/29/former-openai-board-member-explains-why-ceo-sam-altman-was-fired.html

- "Sam Altman no longer owns OpenAI Startup Fund." Axios, April 1, 2024. https://www.axios.com/2024/04/01/sam-altman-openai-startup-fund

- "The real story behind Sam Altman's firing from OpenAI." The Wall Street Journal via AIC, 2025. https://aicommission.org/2025/03/the-real-story-behind-sam-altmans-firing-from-openai/

Reddit, Oklo, io, Merge Labs

- "OpenAI inks deal to train AI on Reddit data." TechCrunch, May 16, 2024. https://techcrunch.com/2024/05/16/openai-inks-deal-to-train-ai-on-reddit-data/

- "OpenAI to Acquire Jony Ive's io Devices Company for $6.5 Billion." Variety, May 21, 2025. https://variety.com/2025/digital/news/openai-acquires-io-iphone-designer-jony-ive-1236405936/

- "OpenAI invests in Sam Altman's brain computer interface startup Merge Labs." TechCrunch, January 15, 2026. https://techcrunch.com/2026/01/15/openai-invests-in-sam-altmans-brain-computer-interface-startup-merge-labs/

- "Sam Altman's resignation from the Oklo board could pay off with a major OpenAI deal." Business Insider, April 23, 2025. https://dnyuz.com/2025/04/23/sam-altmans-resignation-from-the-oklo-board-could-pay-off-with-a-major-openai-deal/

- "Sam Altman steps down as Oklo board chair, freeing nuclear startup to work with more AI companies." CNBC, April 22, 2025. https://www.cnbc.com/2025/04/22/sam-altman-steps-down-as-oklo-chair-freeing-nuclear-company-up-to-work-with-more-ai-companies.html

November 2023 firing and the New Yorker investigation

- "Removal of Sam Altman from OpenAI." Wikipedia, accessed April 2026. https://en.wikipedia.org/wiki/Removal_of_Sam_Altman_from_OpenAI

- "'Pathological liar': New Yorker probe details allegations against OpenAI CEO Sam Altman." Ynet News, April 2026. https://www.ynetnews.com/tech-and-digital/article/s1f297i3bx

- "Anonymous Sources Detail Sam Altman's Alleged Untrustworthiness in New Report." Gizmodo, April 2026. https://gizmodo.com/anonymous-sources-detail-sam-altmans-alleged-untrustworthiness-in-new-report-2000742847

- "Why was OpenAI Chief Sam Altman fired in 2023." Storyboard18, April 2026. https://www.storyboard18.com/trending/why-was-openai-chief-sam-altman-fired-in-2023-report-mentions-sociopath-label-lying-allegations-94620.htm

- Hagey, Keach. "The Optimist: Sam Altman, OpenAI, and the Race to Invent the Future." Reported in BusinessToday, March 30, 2025. https://www.businesstoday.in/technology/news/story/inside-sam-altmans-openai-ouster-the-untold-india-link-in-the-november-2023-firing-and-reinstatement-469982-2025-03-30

The October 2025 restructuring and IPO path

- "Our structure." OpenAI, October 28, 2025. https://openai.com/our-structure/

- "OpenAI completes its for-profit recapitalization." TechCrunch, October 28, 2025. https://techcrunch.com/2025/10/28/openai-completes-its-for-profit-recapitalization/

- "What you need to know about the OpenAI restructure." Transformer News, October 29, 2025. https://www.transformernews.ai/p/what-you-need-to-know-about-the-openai-restructure-sam-altman-pbc-foundation

- "Who Owns OpenAI? Complete Ownership Breakdown (2026)." AI Funding Tracker, February 10, 2026. https://aifundingtracker.com/who-owns-openai/