The State Changed Clients But Not Its Size

With states having larger budgets than ever why does everything feel like it is falling apart? This article examines what has shifted and why.

The government is spending more money than at any point in modern history, and nothing works. Emergency rooms have six-hour waits. Bridges are held together by engineering optimism and deferred maintenance budgets. The tax agency has been defunded to the point where a billionaire is less likely to be audited than a single mother claiming earned income credits, a system so perfectly inverted that if you described it to someone who'd never heard of it they'd assume you were making a point about corruption in a country they couldn't find on a map. Both of these things, the record spending and the visible decay, are true at the same time, and that should be embarrassing for both sides of the only argument about government that the political class seems willing to have. The right says the state is too big. The left says the state has been hollowed out. And for forty years this argument has generated enormous heat, furnished entire careers, and changed absolutely nothing about the direction of government spending, which should tell you something about whose interests the argument itself protects.

The right's position is the simpler one to deal with, because it runs headfirst into arithmetic and doesn't seem to mind the bruise. OECD government spending has more than doubled as a share of GDP since 1960. The U.S. federal government spent $6.9 trillion in fiscal year 2024, roughly 24% of GDP. The British state spends more on welfare as a percentage of GDP than it did before the financial crisis. The budget is large, the right is correct about that, but the right's proposed solution has been to cut taxes on the people who already pay less than they should and then act baffled when the deficit doesn't close, like a man bailing water out of a boat he keeps drilling holes in.

The left's explanation is more interesting and more wrong in a subtler way, the kind of wrong that sounds like understanding but stops one step short of it. The institutions were hollowed out, the left is right about that, the regulators are playing cards with the people they're supposed to be watching, and enforcement has been gutted with the quiet efficiency of someone who needs the security cameras to malfunction but doesn't want it to look deliberate. Where the left's story falls apart is in calling the hollowing a shrinkage, because the state kept growing the entire time it was being hollowed out, the way a tree can look healthy from the road, bark intact, canopy full, while the inside has been eaten away by something patient that never announced itself and never needed to. More than 85% of government spending growth between 1970 and 1997 went to pensions and healthcare, costs that rise on demographic autopilot as populations age. The categories that actually serve working-age people, unemployment support, housing, education, were flat or declining as a share of the total, like tenants whose rent stays frozen while the building around them gets renovated for someone else.

Where the money actually goes

The standard defense of all this spending runs like this: Social Security lifts 22 million Americans above the poverty line every year, the NHS provides universal healthcare, and European welfare states offer the kind of parental leave that Americans can only read about with the wistful expression of someone studying a restaurant menu through the window, knowing they can't afford anything on it and the restaurant closed twenty minutes ago.

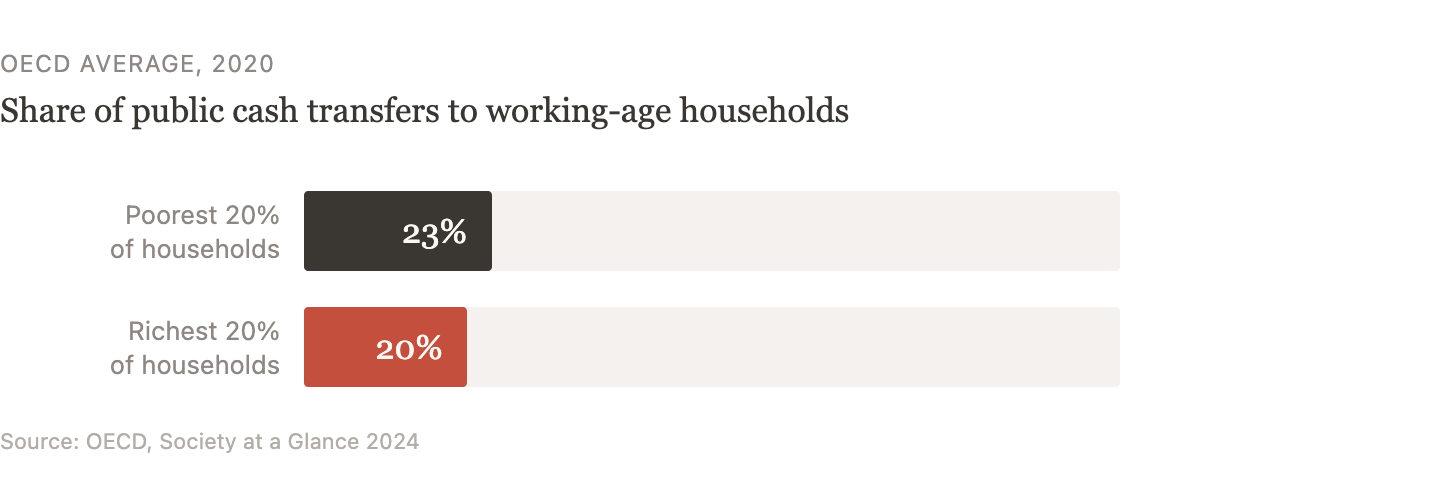

All true, none trivial, and none of it answers the question of who the money is actually reaching, which is where the conversation gets uncomfortable enough that most politicians quietly change the subject. The OECD's own data found that only 23% of public cash transfers to working-age people went to households in the bottom fifth of the income distribution, while 20% went to households in the top fifth, a ratio so absurd it sounds like a misprint until you check the footnotes and discover it isn't, that the welfare state really is handing almost as many bags to the richest family on the street as to the poorest and then publishing an annual report about what a tremendous job it's doing.

The American version of this trick is particularly elegant, because it hides the upward redistribution inside the tax code where most people never look and where the beneficiaries would very much like them to stay. Tax expenditures, the deductions and credits that function identically to government spending but aren't called spending because the people who benefit from them would rather die than be associated with the word welfare, total over $1.5 trillion a year. The 401(k) tax exclusion sends 60% of its benefits to the top 10% of earners, which means a retirement subsidy designed to help ordinary workers save for old age has been quietly repurposed into a tax shelter for people who were going to be fine anyway, like a food bank that accidentally became a Waitrose. Capital gains are taxed at 20% while wages are taxed at up to 37%, which means the income you get from owning things is treated more gently than the income you get from doing things, a tax code authored by people who have evidently never done things for a living. The state built a welfare system with two entrances: one at the front with a means test and a waiting room, one at the back with an accountant and a handshake. Most of the money flows through the back, and the people going in that way have never thought of themselves as recipients of government largesse, a cognitive trick that must be nice.

Nobody planned the river

The political scientist Mancur Olson explained half a century ago, in a book called The Logic of Collective Action that most politicians have never read and all of them have lived, why this distribution is a structural inevitability rather than a conspiracy: a $1 billion policy change that benefits 100 corporations by $10 million each will be lobbied for with the intensity of a custody dispute, while the same cost spread across 330 million citizens at $3 each will generate the political resistance of a parking ticket that fell behind the fridge.

The most common objection to the "changed clients" framing is that nobody sat in a room and decided it, that there was no memo, no meeting, no villain twirling his moustache. And that's true, in the same way that nobody plans a river but the canyon shows up regardless. The state responded, rationally and incrementally, to the incentives in front of it: older populations vote more reliably than younger ones, concentrated interests lobby harder than diffuse ones, campaign donors get meetings and constituents get form letters. Each decision was individually defensible, each compromise was made in good faith by at least some of the people making it, and the cumulative effect was a forty-year transfer of resources from people who work to people who own, carried out in broad daylight by people who would be genuinely offended if you described it that way.

The corporate side of this transfer is documented separately, where $4 trillion in profits and $1.57 trillion in shareholder returns coexist with 245,000 tech layoffs and stagnant wages, the private sector's version of the same client switch.

The fact that nobody planned it does not mean the canyon isn't there, and the political system's inability to reverse it comes from the same place it came from, because the incentives that carved the channel are the same incentives that would have to be overridden to fill it back in, which is like asking the river to flow uphill because the people downstream have started complaining about the flood.

The bipartisan receipt

If you wanted to watch the state serve its actual clients in real time, the 2008 financial crisis was the equivalent of catching your partner's text messages and having to reinterpret the last three years of working late. Governments mobilized $2.5 trillion in central bank asset purchases in a single quarter and authorized $700 billion under TARP to rescue institutions whose executives couldn't explain their own balance sheets, a speed and generosity that was never made available to the homeowners those same institutions had spent the previous decade selling mortgages the way a street vendor sells watches, quickly and without too many questions about provenance. The median American household lost roughly 40% of its net worth between 2007 and 2010, and forty-seven bankers went to prison globally for crisis-related conduct, over half of them from Iceland, a country with the population of Coventry, which tells you less about Icelandic criminality than about the relative independence of the people doing the investigating everywhere else.

What matters for the argument is that both parties supervised the rescue and both parties ensured the recovery flowed upward, like champagne poured into one of those absurd glass pyramids at a wedding where only the top tier fills up and everybody else stands around watching. Quantitative easing, pursued under Obama and continued by the Fed for over a decade, worked by inflating asset prices, which is a polite way of saying it made the people who owned assets wealthier while everyone else watched the same recovery on television. The Institute for New Economic Thinking found that QE's positive effects on employment and mortgage refinancing were swamped by the dis-equalizing effects of equity price appreciations, which is the economic equivalent of mopping the kitchen floor while the upstairs bathroom floods through the ceiling.

The program's real purpose was to "foam the runway" for the banks.

Obama's foreclosure relief program, HAMP, promised to help three to four million homeowners and managed about a million, roughly a third of whom re-defaulted. Treasury Secretary Geithner told Senator Elizabeth Warren that the program's real purpose was to "foam the runway" for the banks, a metaphor so revealing that it barely counts as one, the homeowners being the foam, squeezed for as many payments as they could manage before losing their homes anyway. In Britain, Tony Blair's Private Finance Initiative wore a different hat but had the same tailor: assets worth roughly £60 billion were built using private financing that will cost taxpayers £170 billion, a gap of £110 billion that flowed to investors while hospitals crumbled and schools leaked, the fiscal equivalent of hiring a contractor who charges you triple, takes thirty years to leave, and bills you for the privilege of watching him do the plumbing wrong. And the carried interest loophole, which lets hedge fund managers pay a 20% tax rate on income that would be taxed at 37% if they earned it by actually working, has been promised for closure by Obama, Biden, and Trump alike, and has survived every one of them with the lazy confidence of a cat that knows it will not be moved from the sofa.

The completed circuit

England's water system is the cleanest test case for where this process ends, because England privatized its water in 1989 while Scotland kept its system publicly owned, giving you the closest thing to a controlled experiment that political economy ever produces outside a textbook.

Since privatization, English water companies have paid approximately £78 billion in dividends to shareholders while simultaneously accumulating over £64 billion in net debt, despite being sold with zero borrowings, a financial achievement that would be impressive if it weren't being performed on the drinking water of 56 million people. They released sewage into rivers and coastal waters for more than 3.5 million hours in 2023. Ofwat's own chief executive admitted that the direction of regulatory error had been "consistently in favour of companies rather than customers" for two decades, and two-thirds of major water companies employ key executives who previously worked at the regulator, which makes the revolving door less a metaphor and more a commuting arrangement between two offices that were never as separate as they pretended to be. Thames Water has asked for a 59% bill increase to fix infrastructure problems caused by decades of deferred maintenance while dividends flowed to shareholders in the Caymans and Qatar, the kind of request that in any other context would be called a shakedown but in the water industry is called a price review.

Scotland, running the public model, charges less, leaks less, pollutes less, and carries no net debt. The efficiency argument for privatization was tested in the one country that ran both systems side by side, and it failed so comprehensively that its defenders have simply stopped mentioning it, the way a family stops bringing up the uncle who bet the inheritance on a horse.

The privatization cycle is the client switch written into contract law: the state builds the asset with public money, defunds maintenance until the service rots, sells it to private operators, and then stands behind those operators as guarantor when they load themselves with debt and tilt toward collapse. The customer pays for the house, pays rent after it's sold, then pays for the roof repair that was deferred while the new owner borrowed against the property to pay themselves. Common Wealth's 2025 Who Owns Britain? project described the business model as one that incentivized asset sweating over asset building, financial engineering over real engineering, which sounds like academic jargon until you remember that "asset sweating" is what your drinking water tasting like the river smells.

What trust looks like when it runs out

The 2026 Edelman Trust Barometer found that 70% of people globally are unwilling to trust someone who differs from them, that the trust gap between high- and low-income groups has more than doubled since 2012, and that only 32% believe the next generation will be better off, numbers that politicians keep blaming on social media the way a chef blames the customers for not enjoying the food. The temptation to treat declining trust as a cultural problem, a failure of civility or attention span or public character, should be resisted, because it flatters every institution that earned the distrust the hard way, by being unworthy of it.

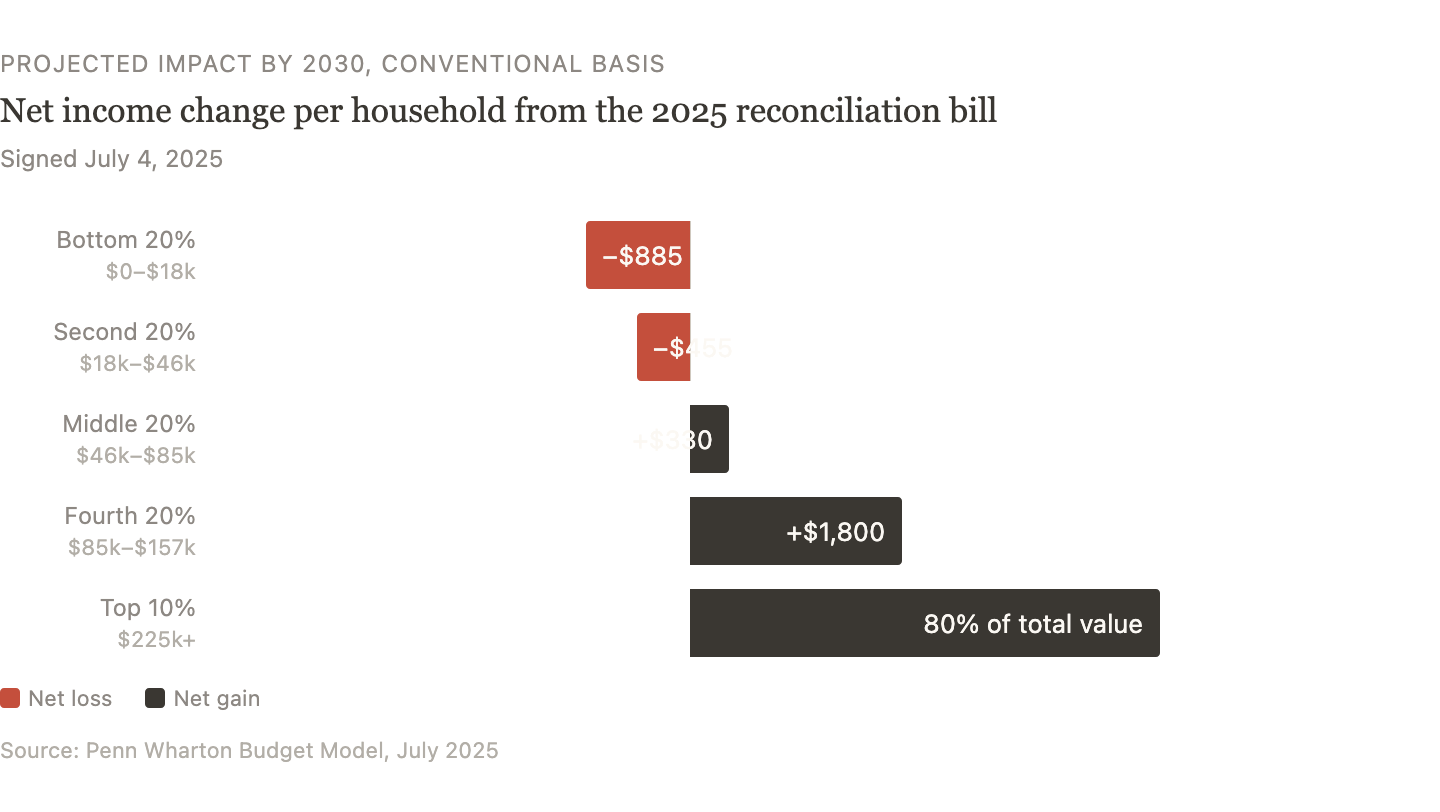

The reconciliation bill signed by President Trump on July 4, 2025, which Penn Wharton found will cost the lowest-income quintile about $885 per household in 2030 while delivering 80% of its value to the top 10%, was signed on Independence Day, which is either the worst scheduling decision in modern American history or the most honest one. The state didn't shrink and the state didn't fail, the state changed clients, and the old clients are starting to notice, which is the point in the story where the people who built the house begin asking why they're paying rent to live in it, a question that every comparable period in history suggests does not get answered quietly.

Whether either party is willing to address this, rather than triangulating around it, is an open question with no encouraging precedent from the current leadership of either side.

Sources

- CBPP, "Where Do Our Federal Tax Dollars Go?", January 2025 https://www.cbpp.org/research/federal-budget/where-do-our-federal-tax-dollars-go

- Resolution Foundation, "Is welfare spending 'out of control'?", November 2025 https://www.resolutionfoundation.org/comment/is-welfare-spending-out-of-control/

- European Journal of Political Economy, "The role of ageing in the growth of government and social welfare spending in the OECD", 2007 https://www.sciencedirect.com/science/article/abs/pii/S0176268006000516

- OECD, Society at a Glance 2024, June 2024 https://www.oecd.org/en/publications/society-at-a-glance-2024_4a3a46d3-en.html

- Curtis, Strine & Webber, "Rebalancing Retirement: How 401(k) Plans Exacerbate Inequality", Harvard Law School Forum on Corporate Governance, September 2025 https://corpgov.law.harvard.edu/2025/09/08/rebalancing-retirement-how-401k-plans-exacerbate-inequality-and-what-we-can-do-about-it/

- Mancur Olson, The Logic of Collective Action, 1965

- Montecino & Epstein, "Did Quantitative Easing Increase Income Inequality?", Institute for New Economic Thinking https://www.ineteconomics.org/research/research-papers/did-quantitative-easing-increase-income-inequality

- ProPublica, "How the Federal Reserve Is Increasing Wealth Inequality", April 2021 https://www.propublica.org/article/how-the-federal-reserve-is-increasing-wealth-inequality

- David Dayen, "Obama's Foreclosure Relief Program Was Designed to Help Bankers, Not Homeowners", Bill Moyers, February 2015 https://billmoyers.com/2015/02/14/needless-default/

- The Conversation, "PFI at 30", December 2025 https://theconversation.com/pfi-at-30-its-hard-to-say-anything-positive-about-this-deeply-flawed-financing-model-195400

- NOTUS, "Trump Wanted to Close This Wall Street Tax Loophole. Republicans Left It Out.", May 2025 https://www.notus.org/money/trump-wall-street-tax-carried-interest-loophole-reconciliation

- Financial Times, Plimmer & Hollowood, water company dividends analysis, April 2024

- We Own It, "Profit from Pollution", June 2024 https://weownit.org.uk/profit-from-pollution

- Common Wealth, Who Owns Britain?, September 2025 https://www.common-wealth.org/publications/who-owns-britain

- Edelman, 2026 Trust Barometer https://www.edelman.com/trust/trust-barometer

- Penn Wharton Budget Model, "President Trump-Signed Reconciliation Bill", July 2025 https://budgetmodel.wharton.upenn.edu/issues/2025/7/8/president-trump-signed-reconciliation-bill-budget-economic-and-distributional-effects