America's reddest state runs a socialist bank

North Dakota votes Republican by margins that make the word landslide sound timid, treats "government overreach" roughly the way other states treat arson, and has owned and operated its own bank since 1919, 3 facts that are supposed to cancel each other out and stubbornly refuse to, because the Bank of North Dakota is real, and by the cold reckoning of S&P Global one of the best-capitalized banks in the United States, which leaves the most reliably solvent financial institution in America sitting in the hands of the most conservative people in it.

This would be an excellent trivia fact if the timing weren't so ironic, but the IMF's April 2026 report put the S&P 500's forward price-to-earnings ratio near a thirty-five-year high, the Magnificent Seven swollen to roughly a third of the index, with most ordinary people's 401(k)s parked right on top of the concentration without their knowing it, a genteel way of saying a great many households have bet the mortgage on seven companies and a hunch about chatbots.

The concentrated risk in those retirement accounts mirrors the concentrated governance problems that let entire industries run on autopilot, nobody asking hard questions until the wheels come off and the damage is already done.

A public bank does nothing for any of that, and this article is not a solution for that problem (before anybody mistakes this for a rescue plan), because when the bubble pops your retirement account falls just as far in Bismarck as in Boston. What grinds a crash into a recession is the thing that comes next, the private banks pulling their lending all at once the way a tide goes out, dragging every loan back to sea so the dry cleaner can't roll over his debt and the wheat farmer can't plant and the woman refinancing her shop is told to come back when the weather clears. That second wave is the one a public bank is built to break.

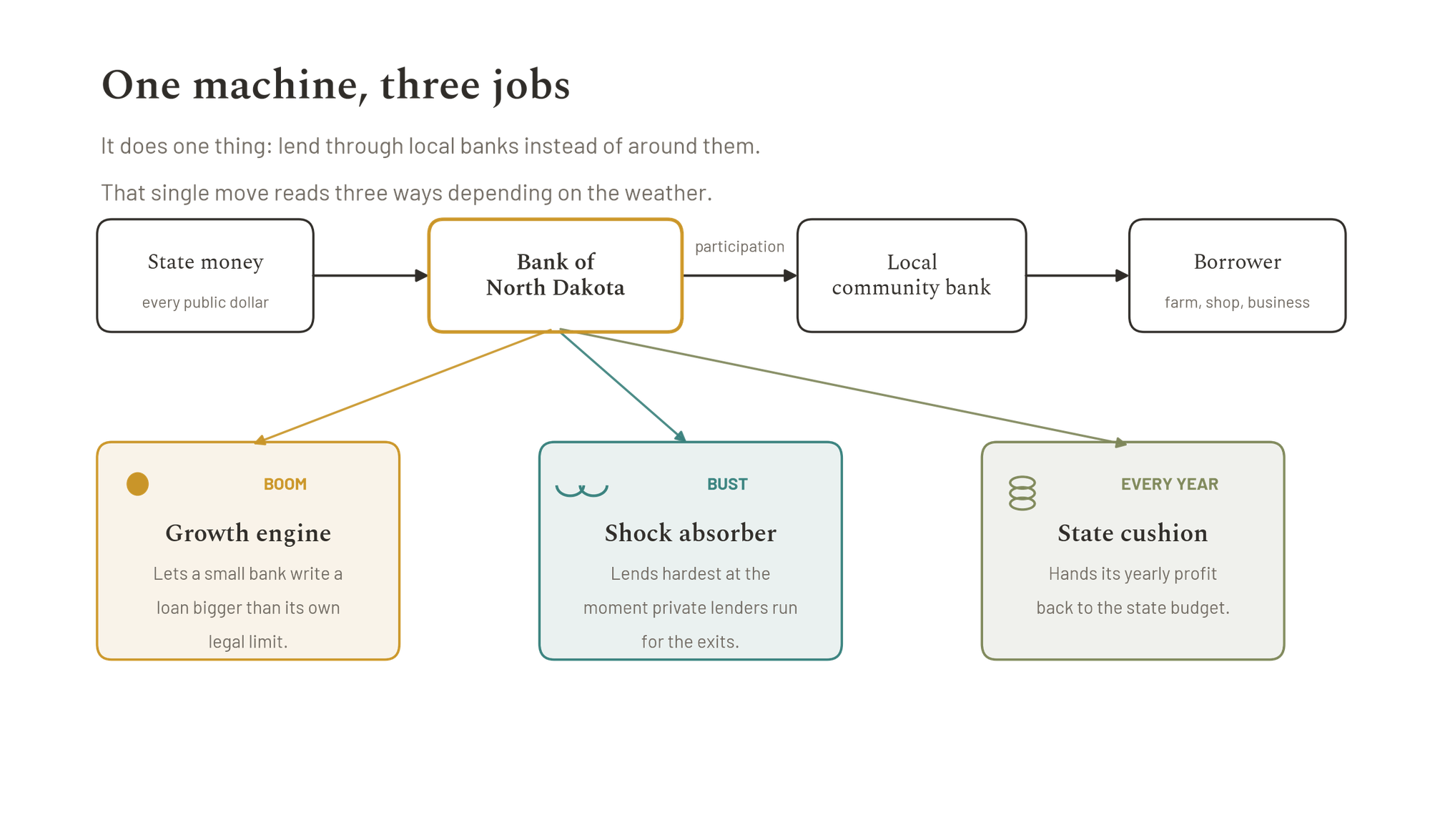

What's strange is how simple the thing doing the breaking turns out to be. The bank only ever does one thing, lend through the local banks, and that single mechanism photographs differently depending on the weather: a growth engine in a boom, a shock absorber in a bust, and underneath both a profit that cushions the state's budget. One machine, three jobs, and the only state running it has been doing so for a hundred and seven years.

A Bank in Bismarck

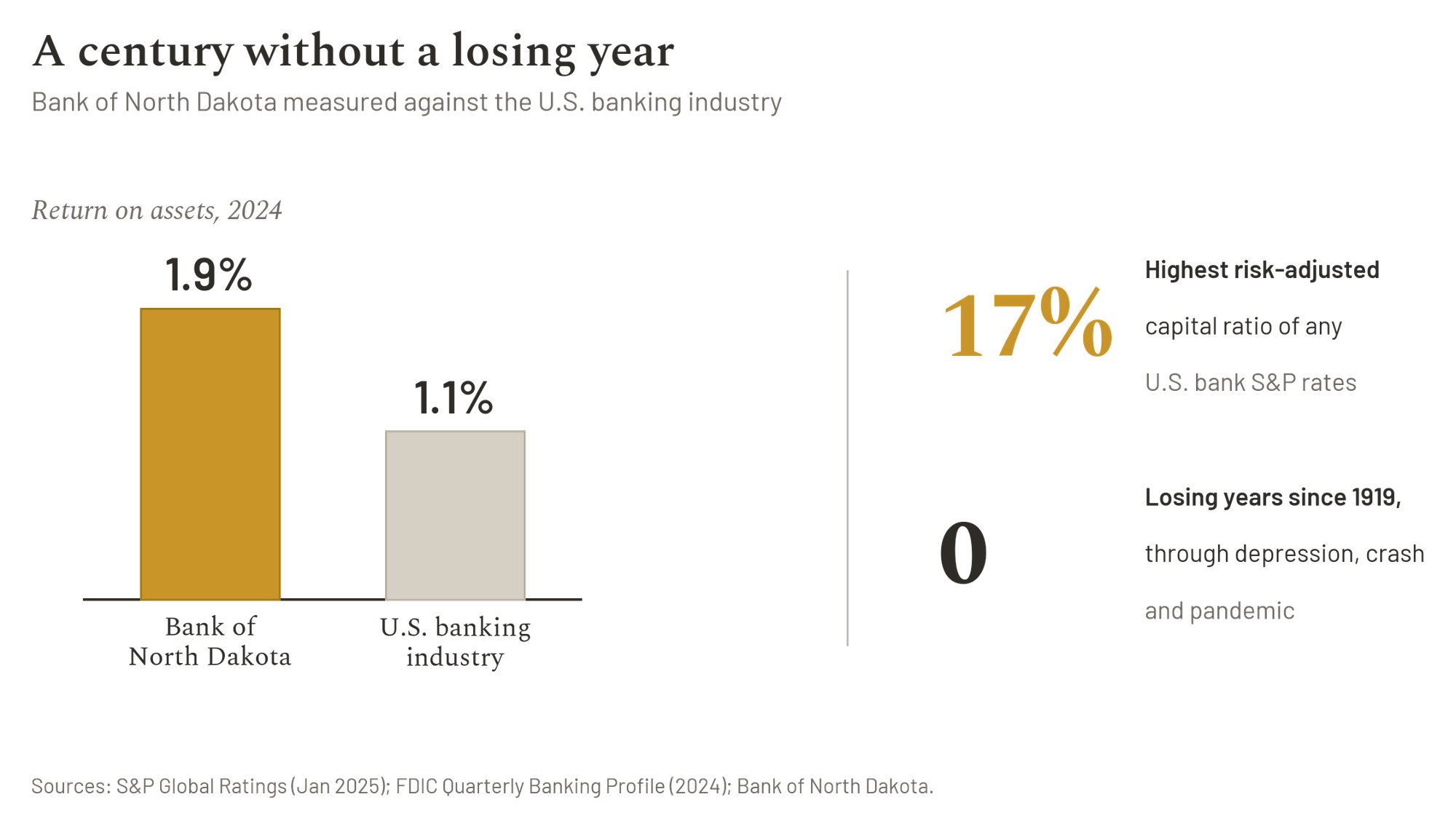

The bank opened in 1919 with $2M and a mandate, and it is still the only one of its kind in the country, a fact usually filed under quirk rather than evidence. It held about $10.8 billion in assets in 2024 and has never once closed a year in the red, not in a farm depression, not in a financial crisis, not in a pandemic. S&P Global gives it the highest risk-adjusted capital ratio of any bank it rates, near 17%, with a return on assets nearly double the industry median and no default in a century, the kind of balance sheet a Wall Street bank would frame and hang in the lobby, sitting instead in a single office in Bismarck that the national debate treats as a rumor rather than an institution with a phone number.

A Farmers' Revolt

Instinct says socialists built it, but the real story is funnier and more American, because the bank came out of the Nonpartisan League, a 1915 movement of furious wheat farmers led by a failed flax grower named A.C. Townley, whose fury had less to do with Marx than with the plain fact that the men who controlled the money all lived somewhere else, charging interest as high as 12% and deciding from back east whether a man could plant. So the farmers won an election, took the legislature in 1918, and chartered the bank, at which point the trusts that had spent decades skimming the state discovered an urgent and principled concern for fiscal prudence, funding the opposition and suing and crying socialism through the Grand Forks Herald, the neatest cover for what had really happened, a lockbox built by people sick of being robbed, with the robbers out front denouncing the lock.

The one mechanism

The mechanism is dull on purpose, and the dullness is the design. Every dollar of state money has to be deposited here, giving the bank a deposit base no private rival can match, carrying a state guarantee instead of FDIC insurance, which makes the people of North Dakota the backstop, for better and worse. No tax, one office, no credit cards, no ATMs, no branches fighting for your checking account, just a wholesale bank that lends through other banks instead of around them, which is why most of the bankers you'd expect to hate it don't. A small-town bank makes a loan and keeps its customer; the Bank of North Dakota buys part of it as a participation, and the two split the risk. The same trick reads three different ways depending on the weather.

The growth engine

In fair weather the trick reads as fuel for everybody else's lending, which is why North Dakota has more community banks per head than any state, roughly six times the national average, and local institutions hold close to 80% of the state's deposits, a number that stops you cold in an era when banking elsewhere has collapsed into four or five names you could fit on a single billboard. A small bank's reach ordinarily ends at its legal lending limit, and that limit is the exact wall the participation model knocks down, the public bank standing behind the private one so it can write a loan it could never carry alone, which is how the PACE program buys down small-business rates by as much as five points, the difference between a storefront opening and a storefront staying boarded up. It reaches the farm gate and the kitchen table too, the same low-rate logic priced into beginning-farmer land and student debt.

The shock absorber

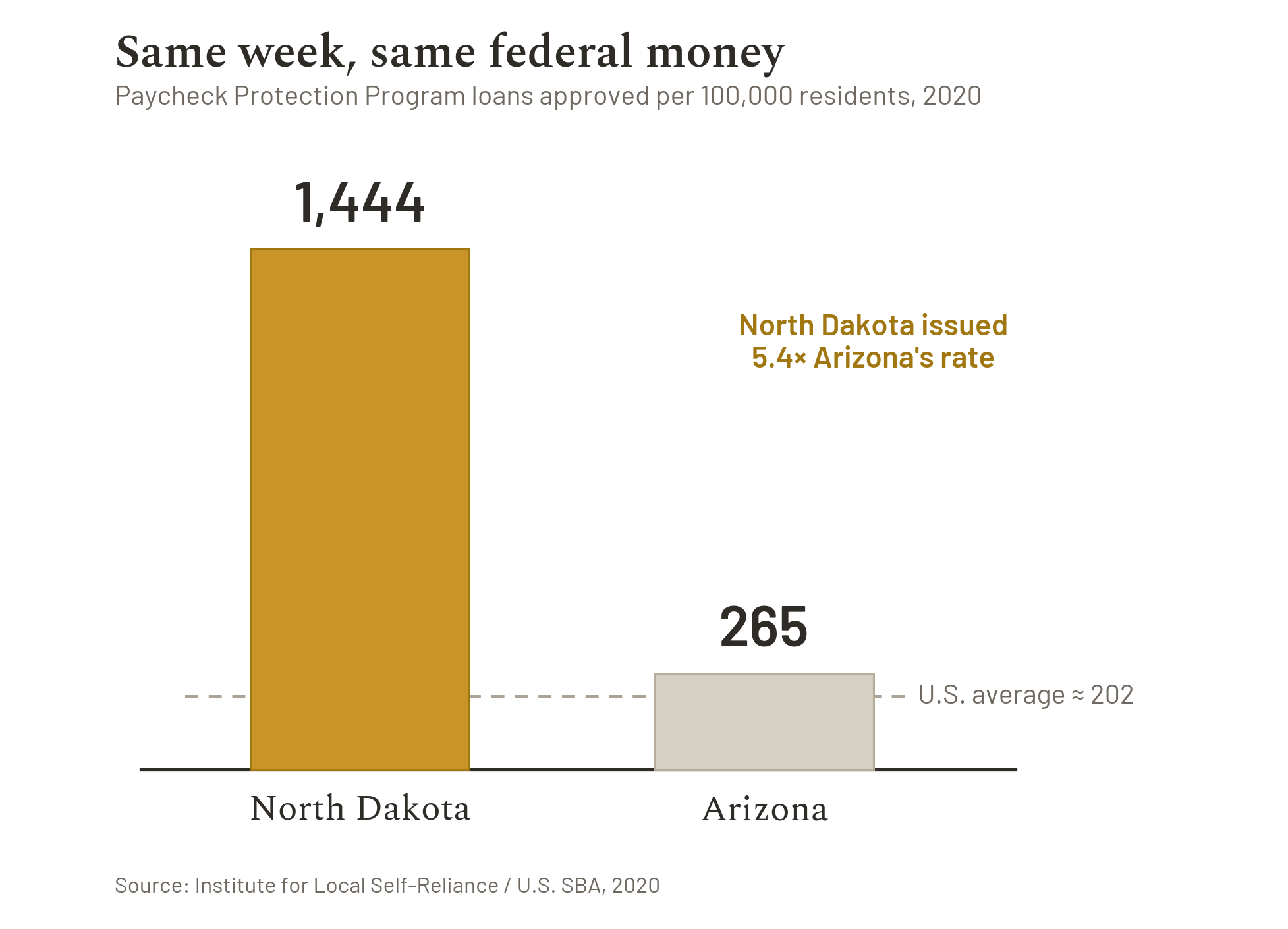

When the weather turns, the same plumbing keeps water moving through pipes that have frozen everywhere else, because the bank lends hardest at the exact moment every private lender is sprinting for the exits, walking into the storm with an umbrella stuffed full of money while the professionals it lends through are still under the awning. Business lending grew 35% between 2007 and 2009, expanding credit in the precise months the rest of the system fainted in unison, and the state was free of the crunch by spring 2009, before the oil boom lazy commentators like to credit for everything good there. The pandemic put it past argument: North Dakota came first of all fifty states in PPP dollars per worker, the bank having packed the state's bags before Washington thought to call the taxi, the result 1,444 loans per 100,000 people against Arizona's 265, the same week and the same federal cash, the difference between a state that owned a bank built to answer the phone and a state that didn't.

The same gap between state capacity and state delivery shows up everywhere you look now, budgets bigger than ever while roads crumble and schools close, the money vanishing into a structure that changed clients but never changed its appetite.

The state's own cushion

The third job is the quietest, and the one budget hawks should like best. Every year the bank hands its profit to the people who own it, a total that has crossed a billion dollars since the first $1,725 transfer in 1945 and reached $228 million in 2023. North Dakota leans on that money about the way other states lean on a rainy-day fund, except this fund refills itself, so in a recession, when tax revenue craters and everyone else is cutting services to the bone, the state has an income its neighbors cannot conjure. Nobody adores it without complaint: Governor Doug Burgum attacked the transfers in 2023 as a raid on money that should have stayed invested, which makes the relationship less a love affair than a long marriage, real and durable and punctuated by fights about the budget.

The honest part

Nothing here ran itself, which the early examiners found out when 191 of 755 farm loans went bad in the 1920s, the favoritism behind them plain. A bank run by the state inherits the state's politics, and in the 1980s farm crisis the shock absorber became a shock amplifier, faltering and deepening the state's mess instead of easing it. A skeptical Washington State treasurer called the model "too much taxpayer risk" in 2018, and he had a point, because with no FDIC the taxpayer is the last name on the hook. The same bank that paid teachers in full through the Depression also helped fund the policing of the Standing Rock protests in 2017, a reminder that a public bank does whatever the public that owns it decides to do, and sometimes the public decides on something ugly.

Too small to copy?

The standard objection arrives on cue, that North Dakota is small and rural and homogeneous, a special case that means nothing for California or New York, an objection that sounds fatal and runs exactly backward, because the engine runs on the partner network and the partner network only gets bigger in a big diverse state. That 1980s failure had one cause, the heavy bet on oil and agriculture that S&P still flags as the bank's single real weakness, the precise concentration a varied state economy would cure, so a public bank in California would sit on a broader, safer loan book and make a sturdier shock absorber. These states already run housing authorities and infrastructure banks; a public bank arrives not as an alien but as a deposit-funded hub bolted onto machinery they already own.

And they are trying. California's AB 857 lets regions charter wholesale, non-competing public banks, which answers the "too big" charge by spreading the work across many right-sized banks, even as Los Angeles alone ships $1.5 billion a year in fees to outside financiers. Yet an LA measure failed in 2018 and bills in Massachusetts and New York keep dying in committee, the latest merely a proposal to study one, which in Albany counts as progress.

Why it never spreads

No new public bank has been chartered in the United States in over a century, and the reason has less to do with the model breaking, which it doesn't, than with it working beautifully for the wrong people, the ones who already own the building and have no intention of installing a second door they don't control. When California debated AB 857 the Bankers Association went straight at it, flanked by the Chamber of Commerce, and New Jersey, asked for a bank, built a $20 million fund and a press release, which is what handing a tent to a family that asked for a house looks like when it's done with a smile. The most revealing opposition is the smallest, because community banks, the very institutions that thrive under the model, routinely fight public banks elsewhere, seeing a competitor where North Dakota's bankers learned to see a backstop. The barrier was never that the thing couldn't be built; it was that a great many powerful people would strongly prefer you didn't.

A century of proof

Everything comes to rest on the one fact that survives every objection, that the Bank of North Dakota has turned a profit every year and has never once defaulted, and the people who own the thing keep it through every swing of the political pendulum, which is why the current Republican governor, Kelly Armstrong, gave the whole game away when he allowed that the bank could never be passed today and then added, "yet we like having it."

The century sits inside that sentence, a bank conceded by the man in charge of it to be something that could not be built now, which means whether a public bank works got settled in 1919, and the only open question left is who gets permission to build the next one.

Sources

The bubble backdrop

- IMF, Global Financial Stability Report, April 2026. https://www.imf.org/en/publications/gfsr/issues/2026/04/14/global-financial-stability-report-april-2026

- Bank of England Financial Policy Committee summary, Oct 8, 2025 (via Hargreaves Lansdown). https://www.hl.co.uk/shares/stock-market-news/company--news/boe-warns-over-risk-of-ai-bubble-in-financial-markets

The bank itself: balance sheet and ratings

- "Bank of North Dakota," Wikipedia. https://en.wikipedia.org/wiki/Bank_of_North_Dakota

- S&P Global Ratings, Bank of North Dakota, Jan 14, 2025. https://bnd.nd.gov/wp-content/uploads/RatingsDirect_BankofNorthDakota_3308011_Jan-14-2025.pdf

- "Bank of North Dakota Outperforms Wall Street," CounterPunch, 2014. https://www.counterpunch.org/2014/11/20/bank-of-north-dakota-outperforms-wall-street/

- Bank of North Dakota, official site. https://bnd.nd.gov/ (see /about-bnd/bnd-operations/, /loans/ag/, /loans/business/, /education-funding/)

Origins and history

- The BND Story (official centennial history). https://thebndstory.nd.gov/

- "Banking on the Government," Federal Reserve Bank of Minneapolis, 1994. https://www.minneapolisfed.org/article/1994/banking-on-the-government

How the mechanism works

- Kodrzycki & Elmatad, The Bank of North Dakota: A Model for Massachusetts and Other States?, Boston Fed NEPPC RR 11-2, May 2011. https://www.bostonfed.org/-/media/Documents/Workingpapers/PDF/neppcrr1102.pdf

- Connecticut Office of Legislative Research, 2010. https://www.cga.ct.gov/2010/rpt/2010-R-0243.htm

- Institute for Local Self-Reliance, "How State Banks Bring the Money Home." https://ilsr.org/articles/how-state-banks-bring-money-home

- Democracy Collaborative, "Community Investment Vehicles" (participation-loan model). https://www.democracycollaborative.org/public-banking

- "The People's Bank," The American Prospect. https://prospect.org/power/people-s-bank/

- ND Legislature, "An Evaluation of the PACE & FlexPACE Loan Programs," Nov 2016. https://ndlegis.gov/files/committees/65-2017/19_5124_03000appendixh.pdf

- "New Bank of North Dakota program allows residents to consolidate student loans," Grand Forks Herald, 2017. https://www.grandforksherald.com/business/new-bank-of-north-dakota-program-allows-residents-to-consolidate-student-loans

The shock absorber: crisis, pandemic, disaster

- ILSR PPP report. https://ilsr.org/banking-consolidation-ppp-report

- "Find out which North Dakota companies got $1.7 billion in PPP loans," InForum (Washington Post), July 2020. https://www.inforum.com/business/find-out-which-north-dakota-companies-got-1-7-billion-in-ppp-loans

- "How a North Dakota bank gave its state a huge lift in the coronavirus small business program," AFLEP. https://aflep.org/how-a-north-dakota-bank-gave-its-state-a-huge-lift-in-the-coronavirus-small-business-program/

- "Disaster recovery for low-income people: Lessons from the Grand Forks flood," Federal Reserve Bank of Minneapolis, 2006. https://www.minneapolisfed.org/article/2006/disaster-recovery-for-lowincome-people-lessons-from-the-grand-forks-flood

- "Bank of North Dakota commits $400 million 'lifeline' to ag producers," North Dakota Monitor, Nov 25, 2025. https://northdakotamonitor.com/2025/11/25/bank-of-north-dakota-commits-400-million-lifeline-to-ag-producers/

- "North Dakota expands low-interest farm loans as applications approach $300 million," North Dakota Monitor, Feb 25, 2026. https://northdakotamonitor.com/2026/02/25/north-dakota-expands-low-interest-farm-loans-as-applications-approach-300-million/

The state's cushion: profit transfers

- "Bank of North Dakota shows record profits; Burgum criticizes general fund transfer," Bismarck Tribune, 2023. https://bismarcktribune.com/news/state-and-regional/govt-and-politics/bank-of-north-dakota-shows-record-profits-burgum-criticizes-general-fund-transfer/article_96db33b2-ff13-11ed-896d-67272970048f.html

The honest part: risks and failures

- U.S. GAO, Financial Institutions: Causes and Consequences of Recent Bank Failures, GAO-13-71. https://www.gao.gov/products/gao-13-71

- "State-owned Bank of North Dakota's unique structure garners attention…," Fox Business (citing 2018 WA Treasurer review). https://www.foxbusiness.com/markets/state-owned-bank-of-north-dakotas-unique-structure-garners-attention-wake-banking-crisis

Can it be copied? The campaigns elsewhere

- Demos, "Putting Oregon's Money to Work for Oregon." https://www.demos.org/research/putting-oregons-money-work-oregon

- California Public Banking Alliance / AB 857 brief. https://capublicbanking.com/ab-857-legislation-brief/ ; https://capublicbanking.org/

- "When, If Ever, Will California Charter A Public Bank?" National Law Review. https://natlawreview.com/article/when-if-ever-will-california-charter-public-bank

- "In California, a Movement for Locally Controlled Finance Gains Ground," Nonprofit Quarterly. https://nonprofitquarterly.org/in-california-a-movement-for-locally-controlled-finance-gains-ground/

- "Does public banking loom in California?" Capitol Weekly. https://capitolweekly.net/does-public-banking-loom-in-california/

- "San Francisco proposal could create nation's first-of-its-kind municipal public bank," Local News Matters, May 25, 2026. https://localnewsmatters.org/2026/05/25/san-francisco-proposal-could-create-nations-first-of-its-kind-municipal-public-bank/

- Jain Family Institute profile (LA history, incl. 2018 Measure B), CB Insights. https://www.cbinsights.com/company/jain-family-institute

- "East Bay Activists Unveil New Blueprint for a Regional Public Bank," Next City. https://nextcity.org/urbanist-news/east-bay-activists-unveil-new-blueprint-for-a-regional-public-bank

- Massachusetts Public Banking, "Our Legislation." https://masspublicbanking.org/202324legislation/ ; https://masspublicbanking.org/

- "The Massachusetts Climate Bank Bill," Berkshire Innovation Center. https://www.berkshireinnovationcenter.com/post/the-massachusetts-climate-bank-bill

- Massachusetts bill HD3247. https://malegislature.gov/Bills/192/HD3247

- New York Public Banking Act A6268 (2025–26). https://www.nysenate.gov/legislation/bills/2025/A6268 ; State Public Bank Commission A7306. https://www.nysenate.gov/legislation/bills/2025/A7306

- NY S01754 (2023, 32 co-sponsors, died in committee), LegiScan. https://legiscan.com/NY/text/S01754/2023

Why it never spreads / the bigger picture

- "How Public Banks Can Meet Public Needs" (Shelterforce, incl. Gov. Armstrong quote), New Economy Project, Apr 2026. https://www.neweconomyproject.org/2026/04/shelterforce-how-public-banks-can-meet-public-needs/

- "What's Next for Public Banking?" Main Street Journal, Dec 2024. https://mainstreetjournal.substack.com/p/whats-next-for-public-banking

- Council of State Governments South, State Public Banks, April 1, 2026. https://csgsouth.org/wp-content/uploads/FAGO-Converted-IR_State-Public-Banks.pdf

- Public Banking Institute (status tracker). https://publicbankinginstitute.org/legislation-by-state/