The AI Layoff Receipts

This article explores do layoffs for AI actually help a business in the long run. We analyze 1000s of transcripts and stock filings to look at the data - the answer is depressing.

The story that roughly 155,000 people were told, across 33 companies, between 2023 and the first quarter of 2026, is that their jobs were being eliminated because artificial intelligence could do the work better, faster, or cheaper, and that the companies they were leaving would emerge leaner and stronger on the other side. It is a story told on earnings calls, in CEO memos, in press releases written with the special tenderness companies reserve for firing thousands of people and calling it progress. We wanted to know if the story was true.

We have written about the productivity gap before, the Klarna reversal, the MIT data showing 95% of enterprise AI pilots delivering no measurable P&L impact, the growing distance between what executives claim on stage and what the research actually finds. Surveys have been suggesting the returns aren't there for more than a year now, and executives in private conversations have been saying the same thing with increasing candor. The worry that AI-driven layoffs are producing no return is no longer contrarian. It is consensus. Nobody wants to say it on the record. What has been missing is the financial proof, the kind that gets audited by accountants, reviewed by lawyers, and filed under penalty of securities law. We went and found it.

We read about a thousand filings (10-Ks, 10-Qs, 8-Ks, the full sediment layer of documents that companies deposit with the SEC) along with 71 earnings call transcripts, for all 32 companies that publicly linked major layoffs to artificial intelligence between 2023 and Q1 2026. We built a dataset, cross-referenced it against the claims, and what the numbers show is not ambiguous: for the vast majority of these companies, there is no demonstrated return on the AI investments that were used to justify the cuts. None. Across three years of quarterly filings, the margins at companies that bought AI and fired people have either stayed flat or gotten worse. The only companies in the dataset with improving margins are the ones selling AI infrastructure to everyone else, and their margins are improving precisely because the companies doing the firing are sending them the savings. Described in any other industry, that pattern has a name, and the name is wealth transfer. In this one, it is called transformation.

The numbers

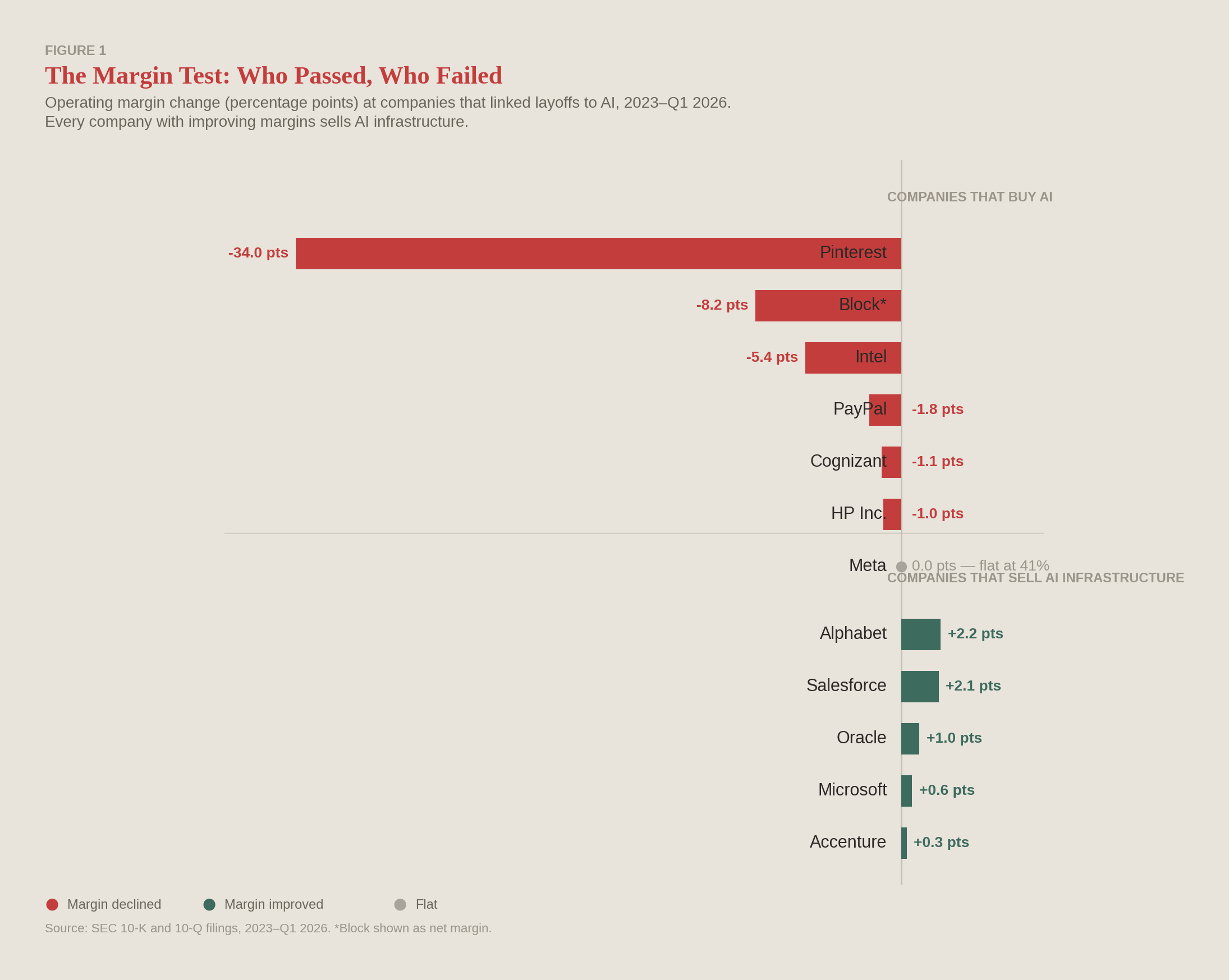

Operating margin is the test that matters here, because it's the one these companies promised to pass: spend less on people, spend some of that on technology, and watch the gap between revenue and costs widen. That was the deal. The filings let you check it against the math.

Where the filings gave us comparable margin data, more companies saw margins decline than improve. PayPal dropped 1.8 points while revenue held steady, which means the company would have been more profitable if it had done nothing at all. Pinterest cratered 34 points, a collapse so severe it suggests the layoffs were a symptom of a deeper problem rather than a cure for one. Intel, which cut 38,800 people in what its own filings describe as a restructuring rather than an AI transformation, is operating at negative 23.1% margins. Cognizant lost 1.1 points on a workforce that actually grew, and HP Inc. lost a full point. Even Meta, whose revenue surged 33%, saw its operating margin slip from 41.5% to 40.6%, because the infrastructure required to run AI at Meta's scale consumes the savings faster than the savings accumulate.

Their revenue was stable or growing, every one of them. The cuts and the AI spending actively made them less profitable than they would have been if they had simply kept the people and skipped the cloud bill. Block's revenue was strong enough to produce a 74% jump in revenue per employee, and it still went from a positive net margin to a negative one. Calling this efficiency is like calling a famine a diet. These companies did not need to cut their way to survival. They cut their way into a vendor's revenue line.

Every company where margins improved sells AI infrastructure, whether that means cloud compute, developer platforms, or enterprise tools. Alphabet gained 2.2 points, Salesforce gained 2.1, and the pattern was already obvious. Oracle picked up 1.0, Microsoft gained 0.6. Accenture gained 0.3 points on an 11,000-person layoff. That is the financial equivalent of rearranging the furniture and calling it a renovation. The margin improvement correlates perfectly with one variable: whether the company sells AI or buys it. The buyers paid for savings they never received, and the sellers recorded those payments as revenue.

The pattern lines up with what the NBER study found when it looked at actual executive motivations rather than press releases, where only 2% attributed cuts to AI capability but 60% cut in anticipation of efficiencies that never materialized.

What the executives say when pressed

When analysts ask for specifics on AI return, the answers turn to vapor. Three years of savings have gone to someone else's income statement, and there is nothing on their own to show for it.

Accenture's CFO, on the company's Q2 FY2025 call, admitted something that deserves to be read slowly: it is still early in the technology, it's still expensive, so you have to get to the right ROI. This from a company that has cut 11,000 people, reported $3 billion in GenAI bookings, and seen its stock drop 28%. A company that sells ROI to clients cannot demonstrate its own. After three years and 11,000 jobs, calling it an early-stage problem is generous. The market has already delivered its verdict, and the stock price is the sentence.

Workday's leadership claimed "significant ROI attached to each and every one" of their AI agents without attaching a number to the significance, and the stock is down 53%, which is the market's way of attaching the number for them. PayPal's CEO said that using AI more extensively "will significantly help us," future tense, zero specifics, on a call where all three margins were down at once. Morgan Stanley's Brian Nowak, on Meta's Q1 2026 call, asked the question that is slowly becoming the defining one of this entire cycle: what are the signposts you're watching to ensure you're actually going to generate a return on all this capital? Nobody answered with a number.

The companies that improved

Amid 32 companies and roughly 150,000 job cuts, the list of businesses that can point to genuine, measurable improvement from AI-linked restructuring fits on a napkin, and even that napkin is mostly companies whose improvement came from selling AI to everyone who was busy firing people to pay for it.

Salesforce is the only non-hyperscaler in the dataset where the margin improvement, the headcount reduction, and a named AI product all line up in the same direction. It cut 4,541 positions, expanded operating margins by 2.1 points, and can point to Agentforce at $800 million ARR growing 169%, customers it can name, deal sizes it can cite. It is one company out of thirty-two, which tells you what the actual odds are of an AI-justified layoff producing a return.

Dell cut 11,000 employees and grew revenue 19%, but the growth came from its AI server business sitting on a $4.5 billion backlog. Dell is selling the picks and shovels; the layoffs and the AI revenue are connected by coincidence rather than causation. Shopify cut 500, held headcount flat, and shipped over 300 new products while its president said AI now writes over 50% of the company's code. But the filing does not confirm the memo: no disclosed AI revenue, a specificity score of 3 in both periods, and a buzzword density that nearly quadrupled.

That is three companies. Out of thirty-two. Two of them sell AI infrastructure, and the third cannot prove the returns in its own margins. The base rate for this bet, if you are a company that buys AI rather than sells it, is effectively zero.

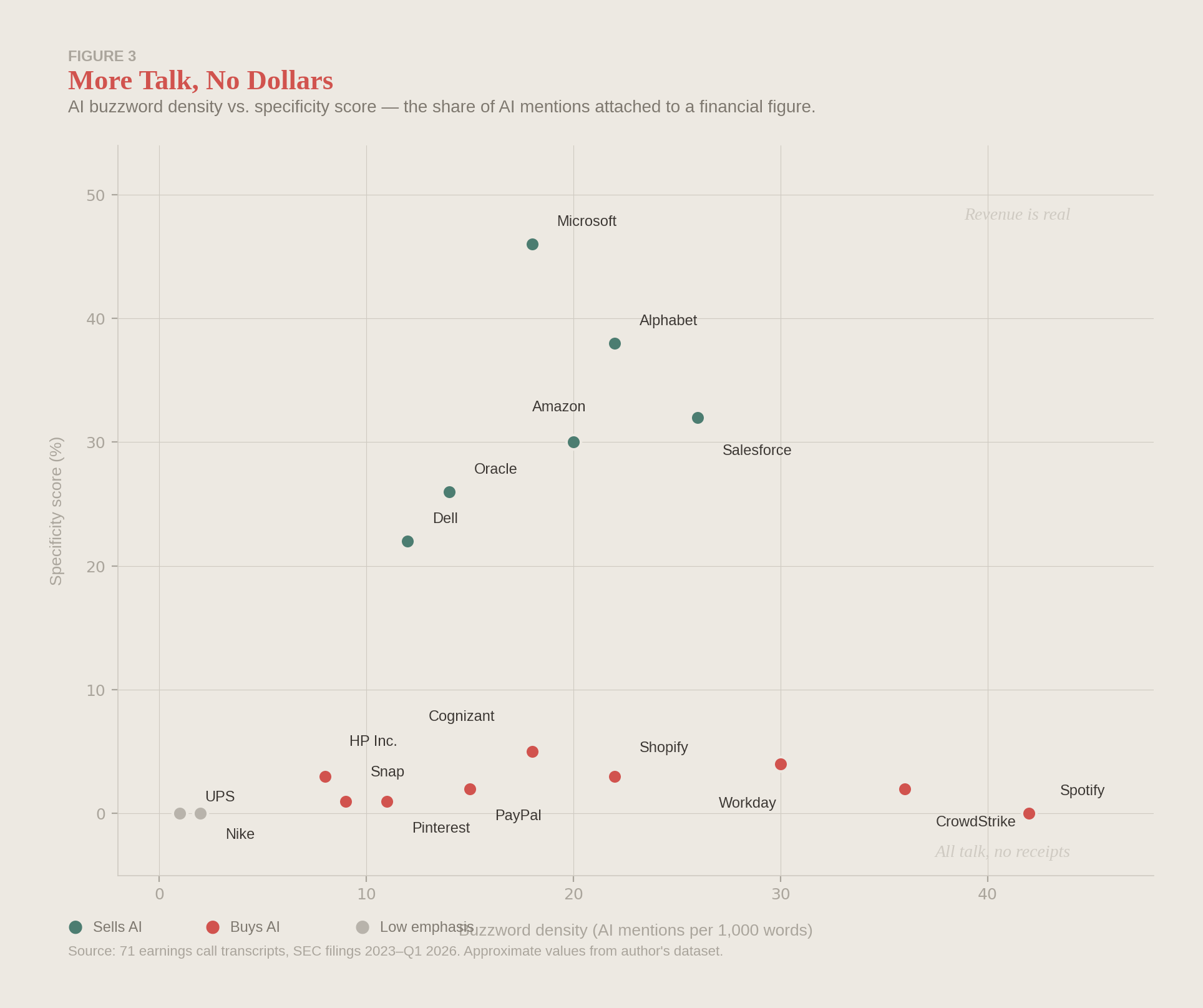

The gap between the word and the number

We tracked every time these companies said "AI" on an earnings call, then sorted the mentions into the ones attached to a dollar figure and the ones floating free. The ratio between those two is what we call the specificity score. Every company with a high and rising specificity score sells AI infrastructure, with no exceptions. Microsoft's score held steady at 45–46 while its raw AI mentions fell, because the revenue is real at $37 billion ARR. On the other side, Spotify's buzzword density rose 3,100% with a specificity score of zero in both periods, meaning 3,100% more AI talk with precisely nothing attached to a dollar sign. CrowdStrike went from 1 AI mention to 102 in a single filing cycle. The filings read like a marketing team discovered a new keyword.

Meanwhile UPS mentioned AI once in its latest transcript, and Nike mentioned it once. These companies cut tens of thousands of jobs between them for ordinary operational reasons, and nobody writes about it, because restructuring without the AI label does not generate headlines. Their margins are fine. Most of the AI-labeling companies cannot say the same.

The direction of the bet

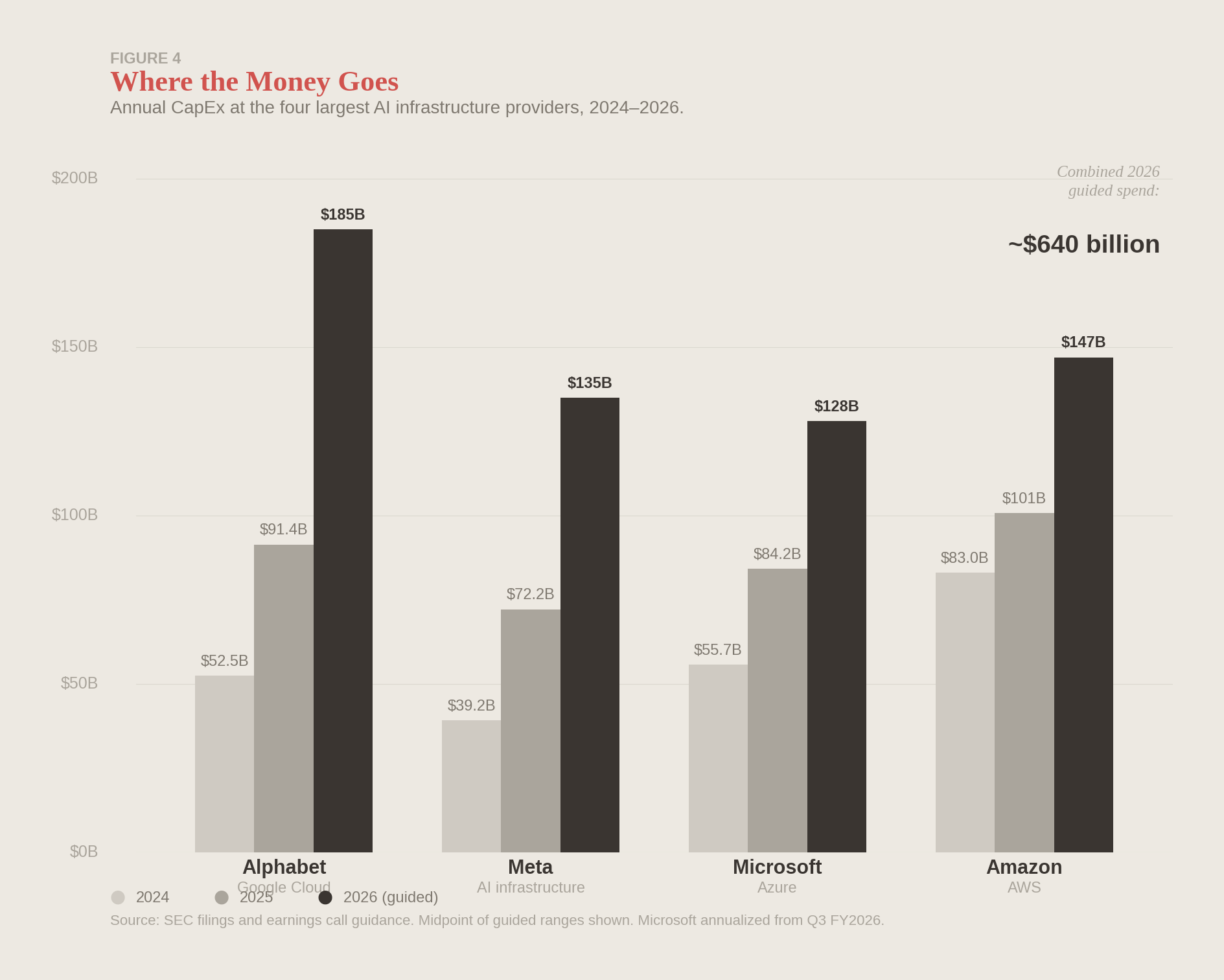

The spending is accelerating even as the returns remain absent: Google guided roughly $75 billion in full-year 2026 CapEx, and Meta guided $125 to $145 billion. Microsoft told analysts it will still be short on capacity through at least the end of 2026 even spending $31.9 billion a quarter, a sentence that would have been science fiction five years ago. Amazon's free cash flow, meanwhile, dropped from $14.8 billion to $1.2 billion, a decline that in any other context would dominate the earnings coverage for a quarter.

Microsoft's CFO was the bluntest about the economics: company gross margin was 68%, down year over year, driven by continued investment in AI infrastructure and growing AI product usage. She described a company that is growing and getting less profitable at the same time, and she described that as the plan, which is an honest thing to say when you are the company collecting the wealth transfer and can afford the patience.

The non-hyperscalers, the companies doing the laying off, are funding this infrastructure build from their payroll lines and getting nothing back for it. Five9's CEO described the mechanism with a clarity that nobody else has matched: AI is replacing humans over time, and those dollars are going back into the software. It is rare to hear a CEO describe the mechanism this plainly. Five9 is small enough to have nothing to lose by saying it out loud. We wrote previously about the bet that corporate America actually made with AI, and it was never productivity. It was permanent wage compression with better PR, a way to gut headcount across an entire economy simultaneously and get applauded for it. The filings confirm the thesis. The money that used to pay a support agent or a junior developer now pays for a cloud computing bill, which pays for a GPU cluster, which shows up as revenue at Amazon or Microsoft or Google. The payroll savings flow in one direction, upward into the income statements of the five companies whose margins are the only ones that improved, and the workers who generated the savings are gone.

Corporate profits hit $4 trillion while companies cut a quarter million tech jobs, returned $1.57 trillion to shareholders, and raised prices on the products those workers used to build, which is a straightforward description of a social contract getting shredded in real time.

The mechanism doubles up on a workforce that was already taking the brunt of these cuts disproportionately, with women representing 25% of tech employees but 45-47% of layoffs and now facing retention criteria based on AI-usage scores they have 22% lower odds of hitting.

Next quarter's earnings calls will put all 32 of these companies back in front of analysts who are, unevenly, learning to ask for the number after the noun. The filings will land and the margins will be what they are.

Sources

SEC Filings

All financial data (revenue, operating margins, gross margins, net margins, headcount, capital expenditure, free cash flow) drawn from SEC EDGAR filings, CIK-verified, for all 32 companies:

- 10-K annual reports (minimum 2 per company, FY2024, FY2025, FY2026 or fiscal equivalent)

- 10-Q quarterly reports (5–7 per company, covering Q1 2024 through Q1 2026)

- 8-K current reports (12–44 per company; earnings releases, layoff announcements, material events)

- 6-K / 20-F filings for foreign issuers (SAP, Spotify)

Specific filings referenced:

- Amazon 10-Q filings, Q2 2024–Q1 2026 (quarterly CapEx trajectory: $11.4B → $25.0B; CapEx at 24.4% of revenue; FCF decline from $14.8B to $1.2B)

- Meta 10-Q filings, Q2 2024–Q1 2026 (quarterly CapEx trajectory; CapEx at 33.7% of revenue)

- Microsoft 10-Q, Q3 FY2026 (CapEx $31.9B; CapEx at 37.3% of revenue; gross margin compression -1.1 pts)

- Alphabet 10-Q filings (CapEx $35.7B in Q1 2026)

- Intel 10-K filings (headcount reduction 124,800 → 86,000; operating margin -23.1%)

- Dell 10-K filings (revenue $95.5B → $113.5B; headcount 108,000 → 97,000)

- Shopify 10-K filings (headcount 8,100 → 7,600; revenue growth +30%)

- Cognizant 10-K filings (headcount 336,300 → 357,600)

- Workday 10-K FY2026 (AI mentions 66 → 138; headcount 20,515)

- CrowdStrike 10-K filings (AI mentions 107 → 139; headcount 10,118 → 10,700)

- UPS 10-K filings (headcount 490,000 → 460,000)

- Okta 10-K FY2026 (CapEx $9M full year)

- Block 10-K filings (net margin +3.1% → -5.1%)

Earnings Call Transcripts (71 total)

Minimum 2 per company (pre-layoff "announcement" period + latest available); 3 for Cisco, HP Inc., Intel, Meta, Okta, SAP, Shopify. All sourced from public earnings call transcripts filed with or concurrent to SEC 8-K releases.

Specific transcripts quoted or cited:

- Accenture, Q2 FY2025 (ACN_FY2025_Q2_ann.txt): CFO on AI ROI — "it is still early in the technology. It's still expensive. So you have to get to the right ROI"

- Accenture, Q2 FY2026 (ACN_FY2026_Q2_lat.txt): CFO non-answer on internal AI productivity; 85,000 AI professionals; plans to hire more entry-level in FY2026

- Meta, Q1 FY2026 (META_FY2026_Q1_lat.txt): CFO on headcount — "headcount optimization efforts in certain functions was partially offset by hiring in priority areas of monetization and infrastructure"; Brian Nowak (Morgan Stanley) question on ROIC signposts; CapEx guidance $125–145B; revenue +33%

- Microsoft, Q3 FY2026 (MSFT_FY2026_Q3_lat.txt): CFO — "Company gross margin percentage was 68% down year-over-year, driven by continued investment in AI infrastructure and growing AI product usage"; $37B AI ARR; 20M Copilot seats; headcount declining; CapEx $31.9B

- Amazon, Q1 FY2026 (AMZN_FY2026_Q1_lat.txt): CapEx and AI infrastructure investment guidance

- Alphabet, Q1 FY2026 (GOOGL_FY2026_Q1_lat.txt): CapEx guided ~$75B full year 2026; Cloud $20B; GenAI products +800%; 60/40 server/data center split on CapEx

- Five9, Q1 FY2026 (FIVN_FY2026_Q1_lat.txt): CEO — "AI is replacing humans over time. Those dollars are going back into the software"

- Five9, Q1 FY2025 (FIVN_FY2025_Q1_ann.txt): Customer labor savings of ~$1.1M/year from single deployment

- Salesforce, Q4 FY2025 (CRM_FY2025_Q4_ann.txt): Agentforce handling 38% of support portal queries autonomously

- Workday, Q4 FY2026 (WDAY_FY2026_Q4_lat.txt): "significant ROI attached to each and every one of them"; CapEx guidance $270M

- PayPal, Q1 FY2026 (PYPL_FY2026_Q1_lat.txt): "leveraging AI more extensively in our development processes will significantly help us"

- IBM, Q1 FY2026 (IBM_FY2026_Q1_lat.txt): 45% developer productivity from internal tool "Bob"; $1.5B AI platform TTM

- SAP, Q1 FY2026 (SAP_FY2026_Q1_lat.txt): 30% developer productivity gain; 20% autonomous ticket resolution

- Shopify, Q1 FY2026 (SHOP_FY2026_Q1_lat.txt): "We shipped over 300 new products and features last year alone. We kept our flat headcount"; AI writes 50%+ of code

- Spotify, Q1 FY2026 (SPOT_FY2026_Q1_lat.txt): Gustav Söderström (Co-President) — "You could translate productivity straight into cost savings and cut headcount, which some companies are doing. We're going to be roughly the same amount of people"

- Twilio, Q1 FY2026 (TWLO_FY2026_Q1_lat.txt): Analyst question — "is there any motion to try to vibe code some of the SaaS solutions yourself in-house?"

- Chegg, Q1 FY2026 (CHGG_FY2026_Q1_lat.txt): CapEx $1M, down 88%

- Intel, Q1 FY2026 (INTC_FY2026_Q1_lat.txt): CapEx guidance increased vs prior expectation

Analysis Datasets

ai_layoff_roi_analysis.xlsx (7 sheets, compiled from SEC filings and transcript analysis):

- Efficiency Metrics — 23 companies, revenue per employee calculations, headcount before/after, revenue growth comparisons

- Profitability Metrics — 23 companies, operating margin, gross margin, net margin, EPS, cash flow before/after layoff periods

- Capital Allocation — 23 companies, CapEx levels and % of revenue, R&D spend, AI revenue/ARR notes, jobs cut, stock performance from layoff announcement to May 7, 2026

- Transcript AI Signals — 71 transcripts, raw AI mention counts, AI + financial specificity scores

- AI Language Evolution — 32 companies, buzzword density (AI mentions per 1,000 words), specificity score changes, workforce mention tracking across periods

- Narrative vs Numbers — 19 companies, alignment assessment between AI narrative claims and financial performance (YES/NO/PARTIALLY)

- Red Flags & Positive Signals — 18 companies, qualitative assessment of AI-washing indicators vs genuine transformation signals

Stock Performance

All stock prices sourced from closing prices on layoff announcement dates and May 7, 2026, as recorded in the Capital Allocation sheet. Notable returns cited: Intel +205%, Cisco +53%, Amazon +46%, Block +24%, Salesforce +14%, Alphabet +11%, Microsoft +7%, Cognizant -5%, PayPal -10%, Pinterest -11%, Oracle -23%, Freshworks -24%, HP Inc. -25%, Snap -25%, Accenture -28%, Workday -53%, Chegg -57%.