The Social Contract Is Broken in America

Corporate profits hit $4 trillion. S&P500 companies returned $1.57 trillion to shareholders. They did this while cutting a quarter million tech jobs and raising prices. This article explores how both corporate America and government broke the social contract and what could come next.

Corporate America is having the best years of its life. Corporate profits hit $4 trillion by the end of 2024, more than double what they were in 2010, and 2.3 percentage points higher as a share of national income than before the pandemic. S&P 500 companies returned a record $1.57 trillion to shareholders in 2024 through buybacks and dividends, with buybacks alone reaching $942.5 billion. Apple spent $104 billion repurchasing its own stock. Alphabet authorised $70 billion. Projections for 2025 put buybacks on track to exceed $1.2 trillion.

They did this while cutting workers. The tech sector shed over 245,000 jobs in 2025 across 783 companies. Microsoft eliminated 15,000 roles while generating nearly $100 billion in earnings. Alphabet laid off thousands while sitting on enough cash to pay their salaries for decades. By early 2026, another 91,000 tech workers had lost their jobs. These were not struggling companies making desperate choices. They were the most profitable enterprises in human history choosing, quarter after quarter, to reward shareholders and cut labour.

Those cuts fell disproportionately on women, who took 45-47% of the layoff burden despite comprising 25% of the workforce.

The mechanism behind the current wave, how AI gave companies cover to compress wages across an entire economy simultaneously, is worth examining separately, because it represents a new chapter in the same story.

Meanwhile, the prices consumers pay have stayed elevated. The EPI found that rising profits explained over 40 percent of price increases between 2019 and mid-2022, compared with profits normally accounting for about 11 percent. The St. Louis Fed confirmed that higher corporate profits have mostly gone to rewarding shareholders via higher dividends. Corporate profits are up. Consumer prices are up. Wages are stagnant. And the people at the bottom and middle of the income distribution are paying for the gains of the people at the top, through higher prices at the checkout, lower wages in the paycheck, and fewer jobs on the board.

And where is government in all of this? Enabling it. The same decades that produced this concentration of corporate wealth also produced the policy environment that made it possible, deregulation, tax cuts skewed to the top, weakened antitrust enforcement, and a campaign finance system that gives corporations outsized influence over the people who are supposed to regulate them. The relationship between corporate power and government power is not adversarial. It is symbiotic. And it is that relationship, the intertwined failure of both industry and governance, that this article is about.

The (brief) Social Contract

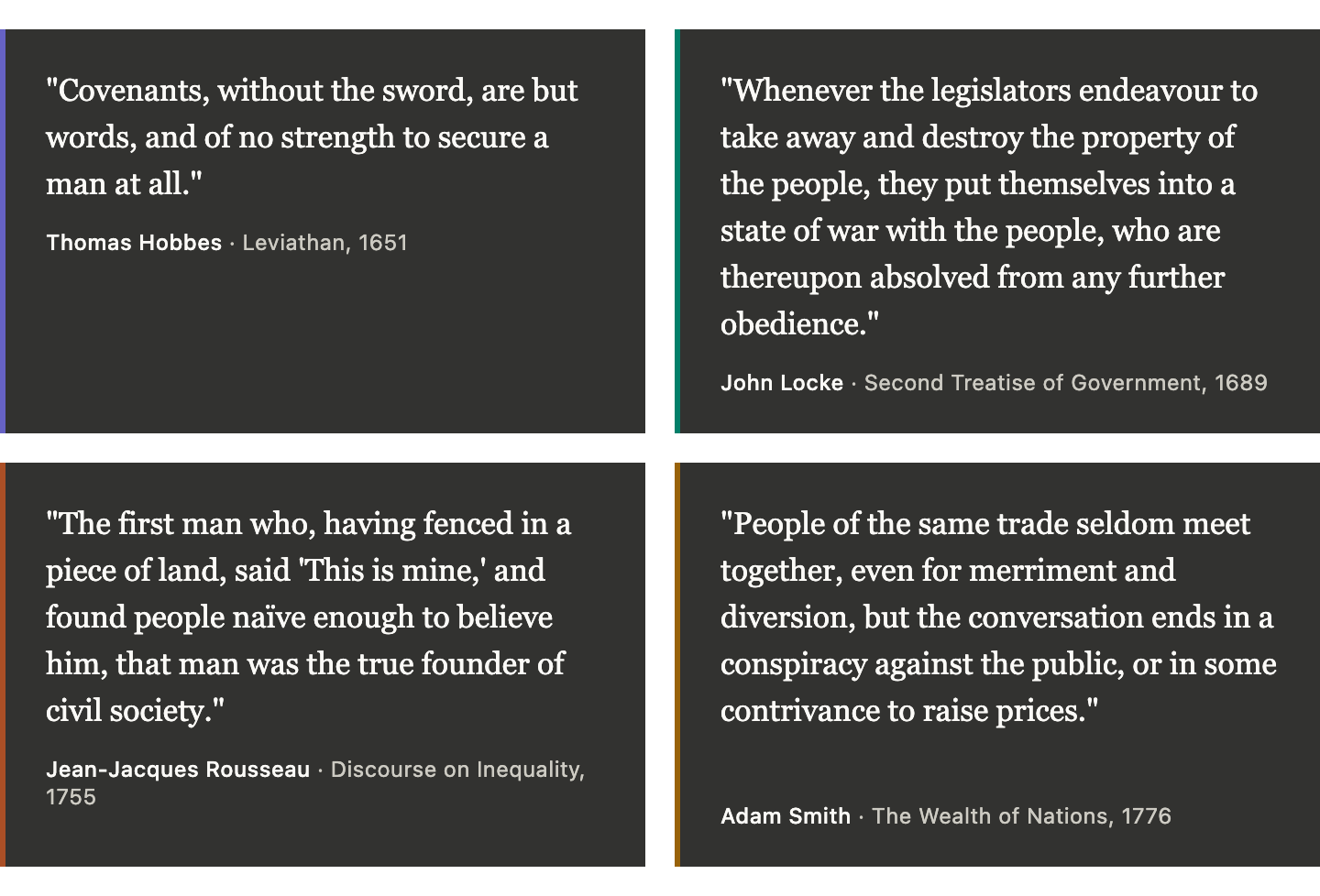

Philosophers have argued about the social contract for centuries, but they share one conclusion: legitimate authority arises from an agreement in which people surrender certain freedoms in exchange for security, rights, and the common good. Hobbes saw this as a bargain born from fear. Locke argued it exists to protect natural rights, and that when institutions fail this duty, the people have the right to dissolve them. Rousseau insisted that any system serving the few at the expense of the many has forfeited its claim to obedience.

These thinkers were describing the contract between citizens and the state. But the same logic extends to industry, and always has. Adam Smith argued that free markets would produce broad societal benefit, but he warned extensively about monopoly, collusion, and the concentration of power among those who would rig the game if unchecked, and he was clear that the state's role was to prevent that rigging. Marx went further: he argued that the bargain between capital and labour was a fiction from the start, that the appearance of voluntary exchange masked a relationship in which workers had no real choice but to sell their labour on terms dictated by those who owned the means of production. You do not have to be a Marxist to recognize that his diagnosis of the power imbalance between employer and employee remains uncomfortably relevant, or that Smith's warnings about concentrated corporate power have been vindicated by the very economy he helped theorize.

The implicit bargain that most working people carry in their heads goes something like this: businesses are granted the freedom to operate and profit, and in return they contribute to societal well-being through fair wages, stable employment, and baseline respect for the communities they operate in. Government, for its part, is supposed to be the referee, setting the rules, enforcing them fairly, and ensuring that the game is not rigged so completely in favour of one side that the other has no meaningful stake in playing. Nobody signed either contract. But together they form the architecture of a functioning society: industry creates wealth, government ensures it is distributed broadly enough to maintain legitimacy, and workers contribute their labour in exchange for a reasonable share of both.

Milton Friedman argued that a corporation's only obligation is to maximise profit within the rules of the game. His position deserves confrontation, not deference, because it contains a fatal assumption: that the rules are fair and were not written by the very interests they are supposed to constrain. In practice, corporations do not merely play within the rules. They fund the campaigns of the people who draft them, employ the lobbyists who shape them, and spend whatever it takes to change them when they prove inconvenient. The 2010 Citizens United decision blew the doors off corporate political spending. The revolving door between regulatory agencies and the industries they oversee ensures that the people writing the rules often have a financial interest in writing them weakly. Friedman's argument is an elegant closed loop: maximize profit within the rules, and also decide what the rules are. In my view, that is not a social contract. It is a unilateral declaration dressed up as philosophy, and it has provided the intellectual cover for forty years of wealth extraction by giving corporations a moral framework in which taking everything they can is not just permitted but virtuous, while any expectation that they give something back is framed as an illegitimate imposition. The result is a system in which corporations set the terms, government enforces those terms on their behalf, and workers are told that the arrangement is freedom.

The Deal That Was

There was a time when the contract worked well enough that nobody needed to think about it. You showed up, worked hard, and received a wage that could support a family, benefits that covered your health, a pension that would carry you through retirement, and a reasonable expectation that loyalty would be reciprocated with stability. Government held up its end by investing in infrastructure, education, and a safety net that cushioned the worst outcomes. Corporations held up theirs by sharing enough of the gains to keep the workforce invested in the system.

In 1980, median household income was $17,710. The median home cost $64,600, three times annual income. A new car cost $7,557. One income could handle a mortgage, a car, and a holiday. By the mid-1990s, median income had reached $34,080 and the home price-to-income ratio still hovered near 3:1. The math worked, and because it worked, the system maintained its legitimacy. People believed the deal was real.

The Divergence

From 1948 through the late 1970s, worker compensation and productivity grew in lockstep. This was not automatic, it resulted from deliberate policy: strong unions, a robust minimum wage, progressive taxation, and an expectation that prosperity would be broadly shared. Government and industry were both doing their part, imperfectly but materially.

After 1979, those lines diverged permanently. Productivity grew 59.7 percent by 2019. Typical worker compensation grew 15.8 percent. The wealth generated by each hour of labour increasingly flowed into executive pay, shareholder returns, and corporate profits.

Some economists dispute this framing, arguing that adjusting both measures with the same deflator narrows the gap, and that total compensation including benefits has tracked productivity more closely. These are fair methodological points. But the worker paying $400 more per month for a health plan with a $6,000 deductible is not experiencing rising compensation in any meaningful sense. Benefits that cost more and deliver less are not evidence the system works.

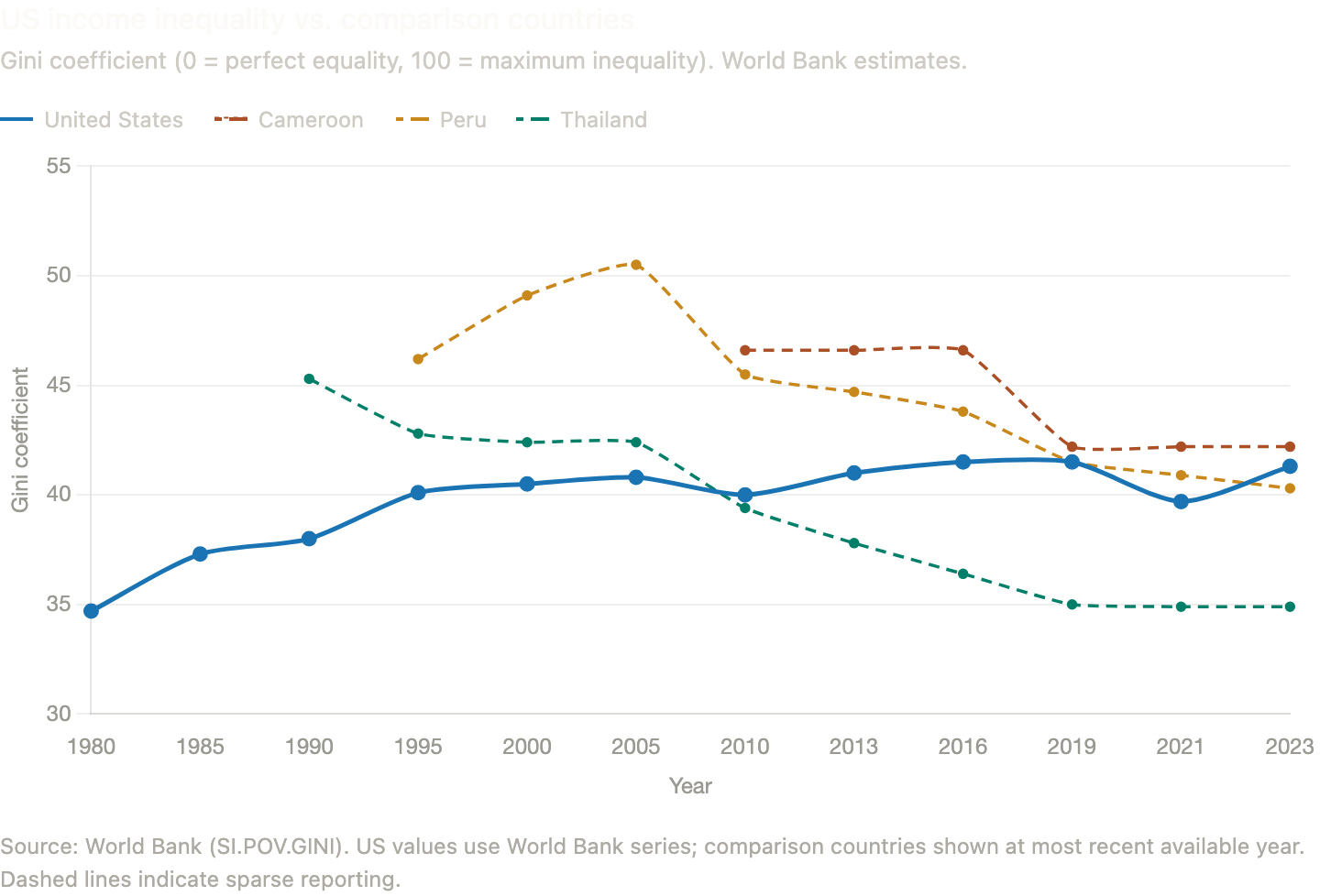

The Pew Research Center showed how gains were distributed. From 1981 to 1990, the bottom 20 percent saw income decline 0.1 percent annually; the top 5 percent gained 3.2 percent. The Gini coefficient, the standard measure of income inequality, where 0 represents a society in which everyone earns the same and 1 represents a society in which a single person holds all the income, crossed 0.40 in 1983, reached 0.43 by 1990, and stood at 0.49 by 2024. To put that in context: the United States now has a higher Gini coefficient than Peru, Cameroon, and Thailand. Rousseau warned that a system serving the few forfeits its legitimacy. He did not need a Gini coefficient. The Gini coefficient proves he was right.

The Dismantling

In 1980, 38 percent of private-sector workers had defined benefit pensions. By 2008, 20 percent did. Defined benefit plans went from 27.2 million active participants in 1975 to 11.1 million by 2023, while 401(k) plans, where you carry the investment risk, ballooned to 96.4 million. When companies switched, contributions per employee were cut nearly in half. The promise was replaced with a suggestion, and the bill was halved.

This was not purely a corporate decision. Government enabled every step. The Tax Reform Act of 1986, the Pension Protection Act of 2006, and a series of regulatory changes made defined benefit plans increasingly costly and volatile for employers while making 401(k)s easier and cheaper to administer. The policy environment did not just permit the shift, it incentivised it. Union membership, the only structural counterweight to corporate power, fell from a third of private-sector workers in the 1950s to below 10 percent today, aided by labour law that failed to keep pace with employer hostility and by decades of political choices to leave it that way.

The government side of this story is its own article, because the state did not shrink during these decades, it grew, but it changed who it serves, and OECD data shows the poorest fifth now receives barely more in transfers than the richest.

The EPI traces the pay-productivity divergence directly to intentional policy: erosion of the minimum wage, weakened labour law, deregulation, tax cuts for top incomes, and macroeconomic policies tolerating higher unemployment. The pattern was always the same, risk transferred from corporation to worker, with government holding the door open, and the whole arrangement dressed in the language of flexibility, innovation, and personal responsibility.

Where This Leads

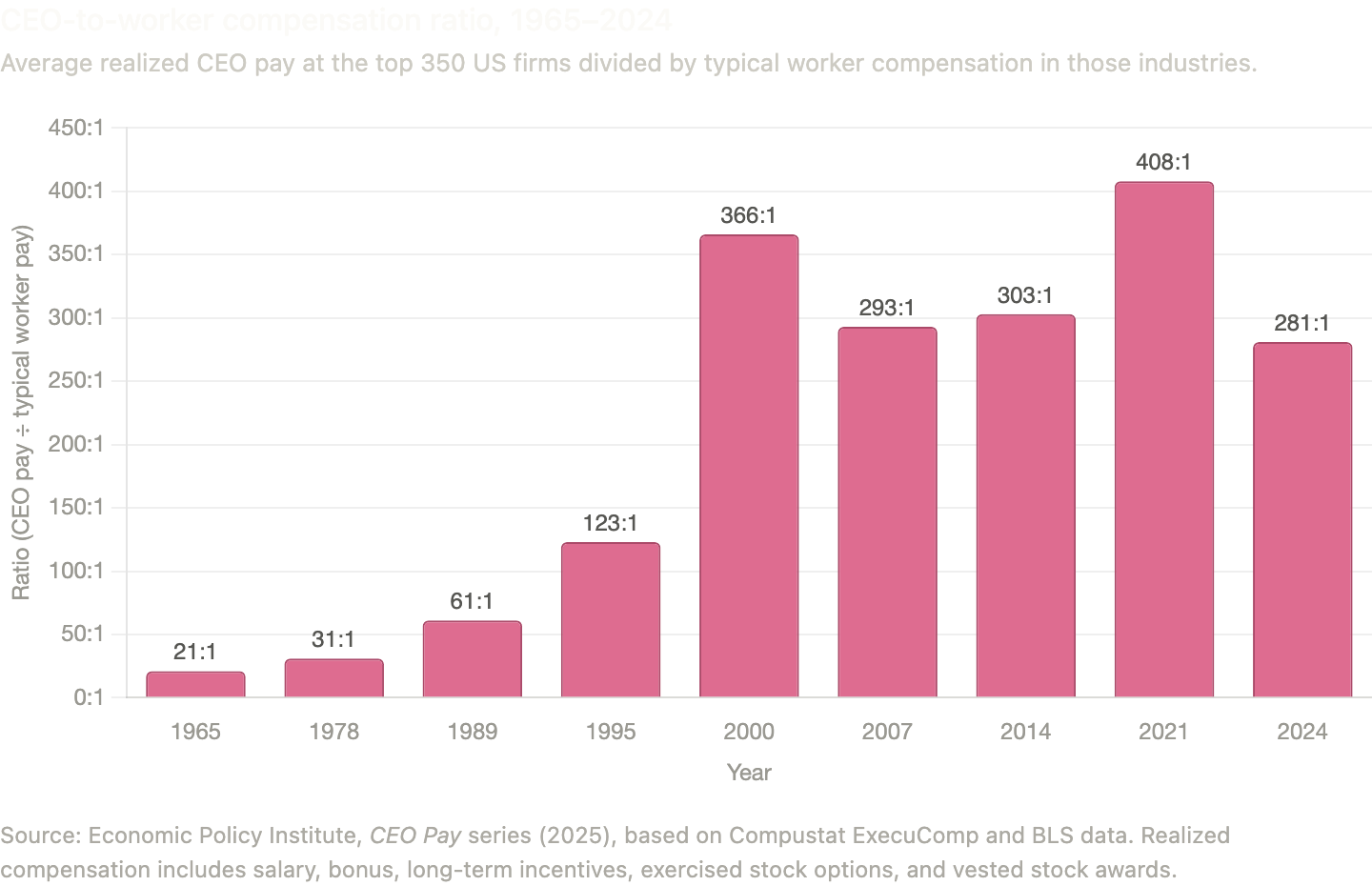

The CEO-to-worker pay ratio was 42:1 in 1980. The wealth gap between the richest 5 percent and the second quintile doubled from 114:1 to 248:1 between 1989 and 2016. The bottom 50 percent hold less than 4 percent of national wealth. The bottom half's income share fell from 20 percent in 1980 to 12 percent by 2014; the top 1 percent's share rose from 12 to 20 percent. In 1981, the top 1 percent earned 27 times the bottom half. By 2014, 81 times.

These are the vital signs of a social contract in terminal decline, and it is a contract that was broken by both parties to it. Corporations extracted. Government permitted. And the people at the bottom and middle of the distribution paid the price for both.

Hobbes warned that when the sovereign fails to provide security, the contract dissolves. Locke said that institutions which fail the people forfeit their legitimacy. History tells us what happens next: people disengage, radicalise, and become receptive to movements that promise to tear down the structures that failed them.

Both major parties claim to champion the working class, and both serve the donor class when it counts. Republican populism lives in rhetoric and scapegoating while its legislation redistributes income upward. Democratic populism has struggled to translate ambition into material improvement. Real median earnings for non-college workers fell 14 percent over forty years. Neither party has reversed a single structural trend, because doing so would mean confronting the corporate interests both depend on, which brings us back to Friedman's closed loop: the rules are written by the people who benefit from them, and the referees are paid by the players.

What America needs is at least one party willing to fight for the 99 percent in legislation, not rhetoric. What it has is two parties competing over which populist theatre is more convincing while the transfer continues. There are glimmers, candidates refusing PAC money, voters recognising that tax cuts have not trickled down, but glimmers are not governance.

If neither party repairs the contract, what happens next? The honest answer is that nobody knows. The American system is structurally hostile to third parties. Internal reform requires courage neither party's leadership has shown. When institutional channels are blocked, pressure builds and finds other outlets. Sometimes peaceful, mass movements, civil disobedience. Sometimes not. The conditions that historically produce upheaval, concentrated wealth, declining living standards, captured institutions, a political class serving other interests, are present today and deepening.

I am not advocating revolution. I am pointing out that the current trajectory leads toward it, and that the window for a peaceful answer is not infinite. What I am advocating for is something that should not be radical: for both government and industry to take the social contract seriously before the people living under its broken remains decide to take matters into their own hands.

The workers who lived through the last four decades did not forget the deal they were promised. They learned that neither side, corporate or political, ever intended to keep it. And when enough people reach that conclusion, the question stops being whether the system can be reformed and starts being what replaces it, a question best answered deliberately, not in the aftermath of the alternative.